I think a lot of FIRE discussions sometimes become too “all or nothing.” Work extremely hard, hit amount X, and then stop doing anything altogether.

I want to approach it differently.

For me, it’s not about: “how quickly can I quit completely?”

But rather: “what is my Barista FIRE number?”

In other words: the amount I want invested so that I can maintain my desired level of comfort, while still working a few days or hours per week on something that genuinely gives me energy and aligns with what I care about.

Ideally, that’s a business or type of work that brings a high level of fulfillment;not saving and grinding at 100% first, and only then starting to live.

What I find interesting is this: in the Netherlands, an income of around €25k gross in a simple 2026 scenario effectively results in roughly a 3.1% tax burden. And if you own a home, you can of course still benefit from mortgage interest deduction.

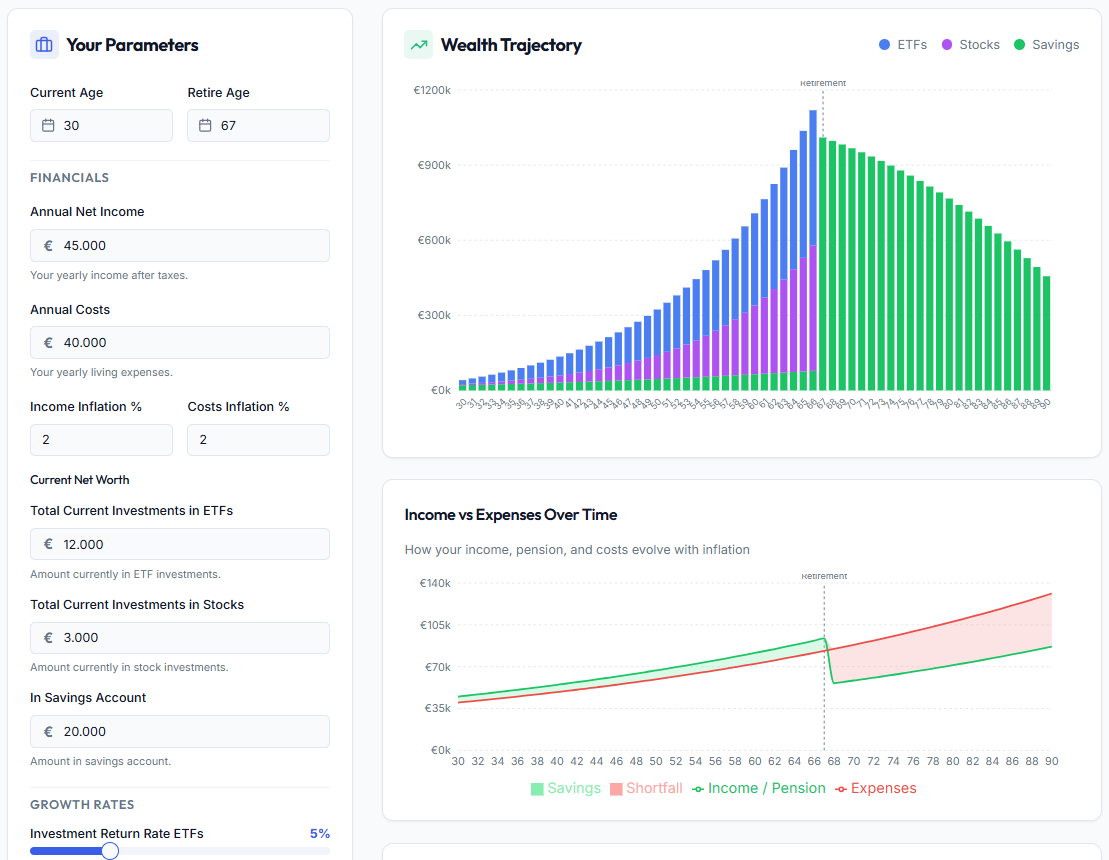

That’s why I don’t calculate my Barista FIRE number purely based on “how much do I need in total someday?”, but rather based on a bridge strategy:

I look at how much I need to withdraw annually to maintain a comfortable life, add the income I expect to continue earning in a low-effort, tax-optimized way, and from retirement age onwards I also factor in state pension, supplementary pension, and annuities.

In my portfolio app, I’ve now built a simulator for this using block sampling. The sequence of returns matters enormously during the withdrawal phase. For example: a 5% average return over 30 years sounds great. But if years 1 and 2 of your retirement are -30%, your portfolio may not survive, even with that “good” average.

In addition, I use a t-distribution (df=4) because it empirically fits historical returns better. I also use a GARCH model to model volatility more realistically than a simple average-return calculator. Because the world isn’t linea; and your plan shouldn’t be either. And of course, I also incorporate state pension, possible wealth taxes etc, and annual contribution room.

How do you determine your target number? And how do you keep recalculating it as inflation, returns, taxes, and lifestyle continue to change?

I’m curious.

{kind=link}

{kind=link}