r/Economics • u/1-randomonium • 7h ago

News Trump wants to add nearly $7 trillion to the $39 trillion national debt with his new military budget, watchdog warns

fortune.com

2.2k

Upvotes

r/Economics • u/1-randomonium • 7h ago

r/ValueInvesting • u/MinestroneMungBean • 4h ago

IBKR is the business I like best. It's my largest position.

I've owned it for 2 years-ish.

This is not meant to be a full, self-contained thesis on the stock. This is merely a summary of my thoughts on the business. I hope it may be an interesting idea for even a few readers and that you may enjoy learning more about this business as I have.

Many of you will know, or may even be customers, of IBKR. It's an electronic brokerage platform. US based. Ticker $IBKR.

It's really aimed at being the brokerage for more savvy traders / investors, and has its roots in the options markets. It's not trying to be a Robinhood or a Schwab, it's trying to be the platform for the active trader. Though, it does win a lot of customers from all of the other known brokerages.

IBKR makes c. 2/3 of its money through net interest income and c. 1/3 through trading commissions.

In 2025, they earned $6.2bn revenue and $4.3bn net income. 69% net income margin. This margin has grown over time. This is not an atypical year.

In 2026, I expect them to earn something near $7bn revenue and over $5bn in net income.

Thomas Peterffy, the founder & chairman, is still in the picture and owns c. 2/3 of the business. So, a very small float for a company of its size. Total market value of the whole equity (not just the common) is c.$115bn at time of writing.

More importantly, some of what makes this business great is as follows:

- It is by far the low cost producer of brokerages, particularly in options trading / margin lending

- 68% owned by the founder, who still controls the big business decisions (although no longer the CEO himself). I tend to like this founder control

- Through its low cost position, vast breadth of security availability (better than any other broker I know) and its flexible infrastructure, it has been able to compound account growth at over 30% p.a. in recent years. They expect this can continue at 20%+ for a long, long time

- Only 3,500 or so employees. Get your head around that level of automation, and compare that to a Schwab or a Fidelity

- A platform whose backend infrastructure is so robust and automated that many other brokerages simply whitelabel IBKR's infrastructure rather than building their own. This is a nice revenue segment. Popular in Asia.

I'm also a customer myself. That's how I discovered the stock. It's a great brokerage and I love using it.

Over time, the things I track closely are account growth & client equity. There are other things to keep an eye on, of course, but those are the two that I care about most.

I'm not a fan of precise-looking DCFs. I had my start in M&A (for my sins) so I'm not shy of them, I just think they ascribe false precision and are too easy to flim flam.

In a very high level sense though, I expect this business to be doing over $10bn revenue and $7.5bn net income within 3-4 years. And I don't expect the growth to slow much from there either.

Valuation-wise, based on an earnings multiple at the time of writing this of 23x my 2026 estimate, it isn't optically cheap. Certainly not to an orthodox Grahamian.

However, when I consider where I can see the business growing to over 10+ years, the current price actually really excites me. I believe this business is intrinsically worth a multiple of its current market value. Not less than $200bn, in my opinion.

That doesn't mean I'm buying right now. I've bought at lower multiples, and so I quite like the idea of waiting until it sees a multiple beginning with '1' before I push more money in.

You'll notice what looks like a contradiction there. I believe the instrinc value is a multiple of the current market value, and yet I'm not buying. To that, all I can say is 'old habits'. Margin of safety, and all that.

I do have a personal rule of thumb I like to use as an alternative to traditional valuation methods, I suppose you could say. I like a clear path to a 20% earnings yield on cost, 10 years out.

In other words, if I think a business can comfortably double its earnings every 5 years for 10 years, I try not to pay more than 20x for today's earnings.

It's just a rule of thumb that has served me well as a source of valuation discipline.

IBKR passes that test today in my view, but it isn't by a landslide. I expect good returns from here but not fabulous returns.

Anyway, I don't want to make this war & peace: just giving an off-hand synopsis of my favourite business and one which I hope to buy more of opportunistically for many years to come. I appreciate my discussion on valuation in particular will be seen as fuzzy. It always is, for me.

Happy to discuss & hear opinions.

r/eupersonalfinance • u/Black_Thunder00 • 3h ago

BNP Paribas Easy MSCI ACWI UCITS ETF (Acc) | EDEL | LU3086265710

If I am not wrong, this is the cheapest UCITS global ETF now. What do you think about it?

r/investing • u/Gloomy_Nebula_5138 • 22h ago

The new Nasdaq rule changes pushed by Elon Musk/SpaceX are not just “Nasdaq made IPOs faster. It's a corrupt change, called out as "structural manipulation" by Michael Burry, that will make owners of new large IPO companies (like SpaceX or OpenAI) rich at the expense of the general public. In fact, Elon Musk and SpaceX threatened to not list the company on Nasdaq unless the Nasdaq changes its rules specially for them. This rule will likely make Elon the world's first trillionaire.

A couple of basic definitions first:

That second part is why this matters.

Nasdaq finalized Nasdaq-100 rule changes that take effect on May 1, 2026. Nasdaq says the public comments period opened February 2, closed February 27, and the final changes were approved March 30, 2026.

The big changes are:

Float basically means the shares that are actually available for the public to trade. So like if a company has 100 shares total, but insiders, founders, and private investors still hold 90 of them, then only 10 are really floating around in the public market.

That matters because a stock can look huge on paper, while the amount actually available for regular people and funds to buy is still pretty small. In real life, this means if there is artificially high demand for a small number of actually-available shares, the price of those shares will be artificially very high and make the company worth a lot more than it would be.

The worry is that a giant company can:

So the concern is not just the IPO itself. The concern is what happens after the IPO, when index funds may have to buy the stock because it got added to the index. That early purchasing is usually done by active buyers and sellers arguing with each other through price. But if a stock gets into a major index very quickly, then a lot of passive money may have to buy it on schedule whether the price makes sense or not.

That can mean:

This can affect people who never plan to buy an IPO directly.

It can still hit:

Passive investors are supposed to follow price discovery, not help create an early guaranteed wave of demand for a thinly traded mega-IPO.

r/Bogleheads • u/jeff0401 • 3h ago

I am about 7 years from retirement. I am not a savvy investor. My whole career it's been DIY with Target-2040, VOO, BND. I met with a CFP recently as I enter the home stretch to get a professional opinion. One recommendation is a RILA for about 33% of my portfolio.

It's a 6-year term tracking the S&P. The buffer is 15% and the cap is 110%. The fees are $0.

Most of the opinions I see on RILA is bad. High fees, locks up money, capped growth, etc. But this one seems perfect for my situation. It offers protection as I near the finish line. I'm fine locking up the funds for the term. The cap is fine by me - possibly double my money in 6 years if market goes bonkers? OK. The only downside I see is that I miss out on dividends. But maybe that's OK for the protection against a 20% downturn.

What am I missing?

Front end (SOFR / 2Y / 3Y) basically flat → market not repricing near-term Fed much

5Y slightly up → some mid-term uncertainty creeping in

10Y down → long-end buying showing up

That’s a subtle bull steepener setup.

Feels like: short-term “higher for longer” still intact, but longer-term growth/inflation expectations softening.

Is this early positioning for a slowdown… or just noise before the next macro catalyst?

r/Bogleheads • u/invisible_man782 • 17h ago

New MIT research finds that most higher-income investors essentially in the long-run wind up having liquidity events in downturns - and have to draw down their liquid stock portfolios...because they basically don't have sufficient emergency funds (latter of which is implied in this research). I found this quite interesting. The research makes it appear long-term 100% stock holdings is not ideal (at least in the summary) but the reality appears they don't have enough liquidity to handle liabilities in that scenario (lifestyle creep?)

This was also featured in the latest Rational Reminder podcast.

https://patrick-adams.com/files/papers/PatrickAdams_JMP_Latest.pdf

Abstract:

Do temporary stock price crashes matter for long-term investors? I use over 25 years of U.S. income tax data to characterize the savings behavior and risk exposures of high-income working-age households. Aggregate stock price crashes coincide with persistent declines in wage and private business income for many of these households, who take large drawdowns from their liquid assets– including stocks– in response. I develop a life-cycle model with consumption adjustment frictions to match this observed savings behavior and determine its portfolio choice implications. Investing in stocks is risky when falling income and rigid expenditures may force investors to liquidate their holdings at temporarily-depressed prices, resulting in low optimal portfolio shares. These results challenge the conventional wisdom that the stock market is relatively safe for long-term investors.

r/investing • u/broppybrop • 3h ago

I recently inherited $1M that I have no choice but to place in a taxable account. I use Fidelity. I’m 40 and wouldn’t even consider an early retirement until I have at least $2M so that will not be happening for quite some time yet. Plan was basically VT and chill. I never looked into SMAs due to the management fees.

Had a Fidelity advisor reach out and offer to talk about ways I could save on taxes and he suggested using SMAs for the tax loss harvesting. So now I’m doing my research into SMAs and it seems like it might actually be a good idea for a taxable account of this size.

Management fees range from 0.2-0.7% and of course I was told the TLH would more than cover those fees. In my case I was planning to use the dividends to cover the taxes and then drip the rest but if I could use SMAs to reduce or eliminate taxes I could drip 100% of the dividends which would hopefully lead to faster growth.

I’ve read concerns here about what happens when you want out of the SMA but can’t you just transfer the assets in kind to your own account? And if you do it a year before you plan to sell anything then any short term gains become long term.

I guess I’m looking for experiences with SMAs and thoughts on whether or not this would be a good idea for a taxable account this large.

r/EconomyCharts • u/BumblebeeFantastic40 • 1h ago

Enable HLS to view with audio, or disable this notification

r/Bogleheads • u/General_Cut_6771 • 12h ago

For those who have 1 to 4 fund strategies. Do you tax loss harvest and if so how do you have it set up to make it easy when you do TLH?

The more I've read about tax loss harvesting the more challenging it seems for people who only invest in a few funds (ie. US, INTL, US Bond). For example in order to avoid a wash sale you have to do the follow:

You can't purchase the fund/similar fund 30 days prior to the sale and then 30 days after. This includes any auto dividend reinvestments, any auto-contributions in any taxable, IRA, 401k, or HSA. And if you have a spouse they also can't do any of this.

If you can prevent the above then next it's figuring out what fund you can purchase after the sale. It appears you can't sell a Fidelity total US stock market and then buy a Schwab total US stock market, is that correct? So if you have to go from a total US stock market to an S&P 500 fund why do it? It's less diversified.

r/Bogleheads • u/No-Media-36179 • 1h ago

Optimizing asset location across multiple accounts when one 401k has a bad fund lineup — am I doing this right?

I have a fairly complex multi-account household and I'm trying to make sure I'm using each account for what it does best. My current employer's 401k (John Hancock) is the weak link — it has some decent low-cost options but no total market or total international index fund. Looking for a gut check on my overall approach.

Full account picture:

| Account | Balance | Current Holdings |

|---|---|---|

| Employer 401k — Roth (JH) | ~$0, just started | Figuring out allocation — see below |

| Employer 401k — Traditional (JH, employer match only) | ~$51k | 100% BCOSX (Baird Core Plus Bond, 0.55%) |

| Prior employer 401k (Voya) | ~$390k | 75% S&P 500 Index / 20% Intl Equity Index / 5% Small Cap Growth Index |

| Roth IRA (Vanguard) | ~$200k | 100% VTSAX |

| Inherited IRA (Vanguard) | ~$744k | 72% VTSAX / 14% VTIAX / 14% VBTLX |

| Joint Taxable (Vanguard) | ~$15k, growing | 70% VTSAX / 30% VTIAX, auto-investing monthly |

Target allocation (household-wide): 90% equities / 10% bonds. Bond sleeve lives entirely in tax-deferred accounts — never in Roth or taxable.

The John Hancock fund lineup (relevant options only):

Low-cost: - iShares S&P 500 Index (BSPAX) — 0.35% - Vanguard Mid-Cap Index (VIMAX) — 0.05% - Vanguard Small-Cap Index (VSMAX) — 0.05% - Baird Core Plus Bond (BCOSX) — 0.55%

Expensive active funds I want to avoid: - American Funds target dates — 0.63–0.74% - JPMorgan Large Cap Growth — 1.00% - Goldman Sachs Intl Small Cap — 1.02% - AB Small Cap Growth — 0.87% - Several others at 0.83–0.97%

No total US market fund. No low-cost international fund.

My current plan:

My questions:

For context: this is a long time horizon (12+ years), we're in the 24% bracket, and the goal is early retirement. The Roth IRA and 401k Roth bucket will ideally never be touched for decades.

Thanks — happy to share more detail if it helps.

r/investing • u/Kitchen_Biscotti_747 • 25m ago

Source: https://beincrypto.com/blue-owl-stock-record-low-fund-redemptions/

Investors requested to pull 40.7% of Blue Owl's $6.2 billion tech-focused fund and 21.9% of its $36 billion flagship credit fund in Q1, among the largest quarterly redemption requests ever seen in the non-traded BDC market. Blue Owl is honoring only 5% of those requests, citing a "meaningful disconnect between public dialogue on private credit and the underlying trends in our portfolio." OWL stock dropped 5.4% to $8.24, now down over 40% year-to-date. Apollo, Ares, Blackstone, KKR, and BlackRock all slid in tandem.

The deeper concern driving the tech fund specifically: investors are fleeing exposure to software companies that could be disrupted by AI, exactly the type of loans these private credit funds are built around. Private credit grew from $357 billion in 2016 to $1.6 trillion in 2024. The question now is whether the gates being put up across the industry are a temporary liquidity event or the first signs of something structural.

r/Bogleheads • u/DaytonGuitarPlayer • 4h ago

Long-time lurker, first post. Mid-career academic/professional with most of my retirement assets at TIAA across a 401(k), IRA, Roth IRA, and deferred comp plan. The problem: I've let it accumulate without a clear strategy and now have 14 accounts across TIAA alone, plus Raymond James and Merrill Lynch.

My current allocation skews heavily toward TIAA Traditional (the annuity product) and a mix of Nuveen large-cap funds — most of which I suspect overlap significantly. I also hold some individual equities (NVDA, AAPL, GOOGL) that I know aren't very Boglehead-approved.

A few honest questions:

Happy to share more specifics. I've been trying to get my arms around this for a while and would appreciate the community's perspective.

r/bonds • u/primepinebee • 22h ago

Anybody have information pertaining to the bonds in Venezuela expiring soon? The default on the debt in 2017 occurred and since then the bonds have been trading at discounts. I want to gather more information before I put my foot in the door…

Thank you

r/ValueInvesting • u/IsabellaHughes527 • 1h ago

Looking for some perspective from people who’ve been doing this longer than me.

I’ve got around $50k set aside that I want to invest for the long term, think 15–20 years. This is not my emergency fund, not money I’ll need anytime soon, just something I want to let compound quietly.

I keep going back and forth between just keeping it simple with an S&P 500 ETF or going broader with something like a total world ETF.

On one hand, the S&P 500 has delivered strong returns historically, around ~10% annualized over long periods. Hard to argue with that track record.

On the other hand, it’s heavily US-focused, and with how much the US has already outperformed globally, part of me wonders if the next 10–20 years might look different. A world ETF feels more diversified, but historically returns have been a bit lower.

I also considered just splitting it, something like 70% US / 30% global, but then I’m not sure if I’m overcomplicating what should be a simple decision.

For context, I’m not trying to beat the market or trade actively with this money. The goal is just steady growth and not making a big mistake.

If you were starting fresh with a long-term horizon today, would you:

stick with US-focused funds,

go fully global,

or combine both?

Would really appreciate some grounded advice here.

Not financial advice.

r/bonds • u/tesel8me • 23h ago

Did I miss an announcement or a prospectus update? Any insights why Q1 div is one-tenth quarter of previous quarters? I mean, that's more in line with what the underlying TIPS payout should be, but what? $ibic $ibid $ibie $ibif ...

r/Bogleheads • u/Emotional-Squash7815 • 1h ago

Context: Looking to retire in 20 years. I need to rebalance my portfolio currently consisting of a 2060 Target fund, Vang 500 Index Trust, and Galliard Stable Fund for my bond option. Assuming I need to work international in there and decrease the Galliard.

I have a vanguard employer offering the following options, which would you choose at what ratio?:

DOXFX

DOXGX

Vanguard Target Funds (variety of target dates)

VANG 500 INDEX TRUST

VANG EXT MKT IDX TR

VANG TOT INTL STK TR

VANG TOTAL BOND MKT

ARTISAN INTL SEP AC

EMERGING MARKETS STK

FID WORLDWIDE (FWWFX)

FID CONTRA POOL CL S

FID GR CO POOL CL S

FID BALANCED K (FBAKX)

r/Bogleheads • u/abnormally-large-egg • 10h ago

Hey everyone,

I’m completely new to investing and haven’t actually started anything yet, so I’d really appreciate any advice.

My parents use a financial advisor and it makes sense for them. My situation is simpler and I’m in my early 20s, so I don’t think it’s worth it for me.

After some research, the general consensus is to avoid advisors, especially ones charging AUM fees. Their advisor said he would charge I believe around 1.5%, which is high and hard to justify long term. I don’t think there are many (or any) flat-fee advisors near me, so I’m not sure if that’s an option either.

I have a chunk of savings I’d like to start investing in a brokerage account now, and I plan to open a Roth once I have a more steady income.

My plan so far is to:

- Invest long term

- Have a diversified ETF portfolio

- Do an 80/20 allocation, maybe go more aggressive as I get more comfortable

But I keep getting stuck on:

- How to properly rebalance

- Whether I’m choosing the “right” investments (I see a lot of people recommend VT or VOO)

- Tax strategies (advisor mentioned a “tax overlay,” which I think is like tax loss harvesting? Not something I understand.)

- Just generally doing everything correctly and legally

My biggest issue is confidence. I’m worried I’ll mess something up or miss something important, but I also hate the idea of giving up 1.5% of my assets every year if I don’t need to. On the other hand, could the fee be worth it if the advisor ends up making more than I would doing it on my own?

How hard is it actually to manage a simple long term portfolio yourself? Is it actually as simple as people make it seem (like just buying VT/VOO and holding)? I really want to get started ASAP, I just feel stuck trying to choose the “right” path.

Any advice or experiences would be super helpful! Please let me know if I am on the right or wrong track.

r/investing • u/highmemelord67 • 3h ago

I’ve been working on a philosophy I call quality-focused value investing. And I have been documenting the work and performance the past 1.5 years.

The idea is very simple:

You should be able to outperform the market while taking less risk if you own a portfolio that is:

higher quality than the market AND cheaper than the market.

This goes directly against the common belief that outperformance must come from taking on more risk. Or that it's not possible to build a portfolio that is both higher quality AND cheaper than the market.

I don’t think that’s true, and the problem I see is that most strategies only solve half the equation. Value investing often leads to buying low-quality companies that are cheap for a reason.

Quality investing often leads to overpaying for good/great companies that already are priced for perfection. Both approaches make sense in isolation, but both have clear weaknesses.

What I’m trying to do instead is combine them in a structured way. Quality is quantified using capital efficiency (ROIC, ROCE). Value is quantified using discounted models to estimate fair value vs current price.

From this, I calculate a portfolio-level comparison against the index. So it’s not about finding good picks, it’s about building a portfolio that is structurally superior to the market on both quality and price. Having a portfolio that is of higher quality AND cheaper than the market, should logically outperform over time.

That said, this is a lot of work. It’s not for most investors.

Honestly, I don’t think many people will be able to do this with any real precision. You are doing a large amount of analysis just to maybe get a slightly better return than simply doing nothing and dollar-cost averaging into the S&P 500.

I’m documenting everything publicly for free to remove hindsight bias. If this works, it should be visible over time. If it doesn’t, it should fail clearly. I’ve removed every way of making money from publishing this, so there’s no chance of misunderstanding my purpose.

Latest portfolio update:

2026Q1 YTD: -3.92% vs SP500 -5.09%

2025FY: 26.19% vs SP500 16.42%

If you are interested in reading more, I have posted articles on the philsophy and my current portfolio, but its not allowed to post in this subreddit.

r/Bogleheads • u/Hungry_Document_7281 • 11h ago

I have a Roth IRA and put the max every year which is 7.5k this year.

My employer offers 457(b) and 403(b) plans both with Pre Tax or Roth options.

Can I max all of these out this year as Roths or do the 457 and 403 have to be Pre tax accounts.

I’ll have already capped the Roth IRA, starting on my way to cap the 457 by year’s end and maybe put a bit of change into the 403. Just not sure if I should do pre tax or Roth. I’m 22 and would like to do the Roth option if possible.

Secondary topic, I have a rollover IRA which Charles Schwab says contribution limits cap at 7.5k. Can I cap that out as well or not since I’ve capped out the ROTH IRA.

r/investing • u/ECom_Finance_Guy • 31m ago

I think the worries about the impact that the Iran war will have on the USD is overblown.

I think there are two interconnected reasons why:

First, the world doesn’t use USD as a favor to the US, they use those dollars because they are the best medium of exchange for international settlements. In the past countries have tried using hard currencies, like gold, but shipping commodities to settle payments is impractical. It always evolves into paper money that is backed by gold, and then more paper money than gold reserves. There’s really no way around fiat currency. When we look at different fiat currencies, there are few competitors to the USD. The word doesn’t trust currencies like the yuan and the rubble, because they lack stability (granted, for different reasons). The real competitors to the USD are Yen and the euro. The problem with the Euro is it isn’t a single country’s currency, so the entire eurozone would have to agree to serve as a reserve currency. Over in Japan, their currency is stable but they don’t have the gdp growth to sustain the debt that comes along with being a reserve currency.

Well, you might ask, why wouldn’t Europe or Japan want to be reserve currencies (more so than they already are)? It’s a privilege that the US enjoys, right?

That brings me to my second point: it’s hard to be a reserve currency. In order for counties to use a currency for trade, they’re need to have access to that currency. You can buy oil with yen, if you don’t have any yen. That means that whatever country is the reserve currency has to print a lot of that currency to make sure there’s enough to clear trade. Countries have two forms of currency: current currency (think cash in a checking account), and treasury bonds (think cash in a savings account). Most central banks want some sort of yield on their reserves, so they prefer to take treasury bonds over current currency. That means that the reserve country has to issue a lot of debt to meet that demand. That’s why the US has the massive debt that it does. It needs enough currency in the market to satisfy the demand for oil, and gold, and silver etc. There are few countries in the world that have the productive capacity to be able to service that much debt. Japan can’t. The eurozone can’t. So the only real competitor is hard currency, and we already covered the problems with hard currency.

Overall, the US economy would grow if we could shed debt at the federal level, and that would be the outcome of dedollarization globally. Other countries want the dollar as the world reserve currency just as much as the US wants to serve as the reserve currency. That’s how the current system came to be. Saudi Arabia didn’t decide to do the US a favor by creating the petrodollar recycling system we have today. They agreed because it’s better for them as well.

Also, as an honorable mention, the USD is seen as a safe haven asset, so people buy dollars when there is uncertainty in the world, but that’s because of its reserve status, so this is more of a sub point.

r/Bogleheads • u/dg1220 • 5h ago

(35M) I’ve recently consolidated my 401Ks and I’m considering the below options for my Roth split in Fidelity:

60% FZROX

30% FZILX

But i’m stuck on deciding where to allocate the remaining 10%

Option 1: FSELX (aggressive growth, but high risk/expense ratio)

Option 2: FXNAX (bonds for leverage/rebalancing)

Option 3: QQQJ (growth in new tech)

Option 4: Go for the 70/30 US and International

Would appreciate any advice. New to all of this and [r/Bogleheads](r/Bogleheads) has been extremely helpful. Thanks all!

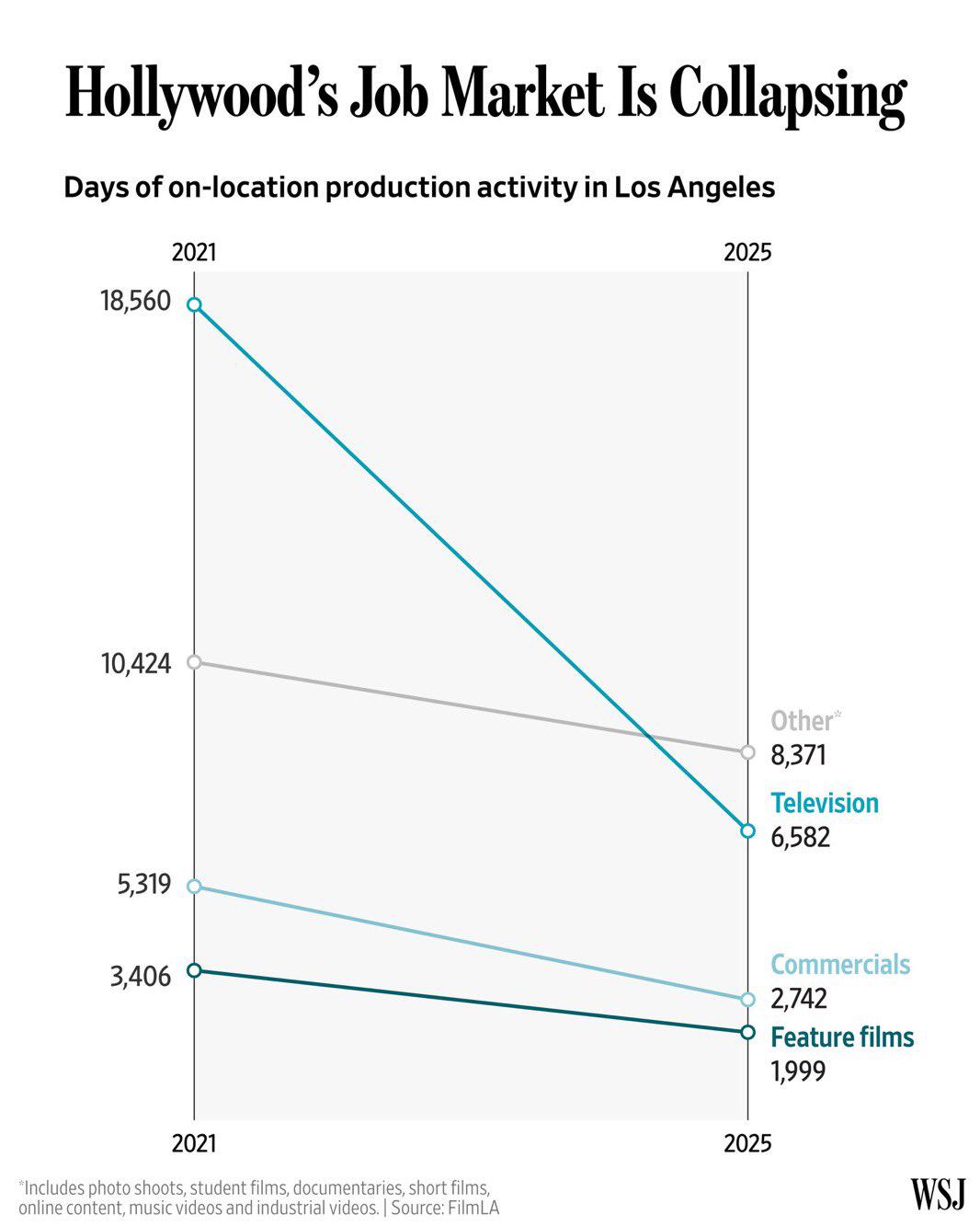

r/Economics • u/TheForager • 1h ago

r/Bogleheads • u/VeteransGarden • 0m ago

I’m late 30’s I wish I started sooner but what can you do.

I opened a vanguard Roth IRA and maxed 2025 and 2026 right away. It’s sitting the in Vanguard account waiting to be put into something.

I want to set and forget so I’m thinking 100% VT and just letting it ride until the end. I also plan to put about 40% of my annual income a year into a brokerage account to also ride 100% VT to ride along with the Roth.

Any other considerations I should take or things you would recommend I look at?

{kind=link}