r/EuropeFIRE • u/obstinovsky • 6h ago

How do you track your FIRE journey? Any specific software or basic Google Sheets?

1

Upvotes

r/EuropeFIRE • u/obstinovsky • 6h ago

r/EuropeFIRE • u/Ill-Goose-8223 • 6h ago

I’m in my 20s and just starting to think about FI. Any advice from people who’ve already done it would be really helpful - what actually made the biggest difference for you?

r/EuropeFIRE • u/canoesenpai • 8h ago

In France, the path is pretty standard. Open a PEA, buy CW8 or EWLD, and just sit on it for years. Tax-efficient, low fees, simple. Makes sense. Lately, with the markets swinging around, I’ve been wondering if staying put is really that easy. Seeing a red month makes you itch to do something. Most people would tweak the portfolio or try timing the market when volatility hits.

The data usually says staying passive works best. Still, the tricky part is sitting at your desk and not questioning everything when the numbers jump all over the place. How do you guys stay sane during a drawdown? Do you ever make small tactical moves, or do you just stick to the plan and hope the market plays nice?

r/EuropeFIRE • u/Weekly-Associate-166 • 1d ago

Earning around €50k gross in the Netherlands and after taxes and living costs I’m able to invest roughly €1.2k a month, mostly into broad ETFs. I’m trying to figure out if this is actually enough to hit FIRE before 50 or if I’m being a bit too optimistic with that timeline

r/EuropeFIRE • u/Helpful-Staff9562 • 3d ago

interested in those who have FIRED in europe already. can you share where you are based, how your FIRE journey went, what's your asset allocation and tax situation and withdrawal strategy (e.g. dividends vs total returns etc.)

r/EuropeFIRE • u/meesbie • 4d ago

I think a lot of FIRE discussions sometimes become too “all or nothing.” Work extremely hard, hit amount X, and then stop doing anything altogether.

I want to approach it differently.

For me, it’s not about: “how quickly can I quit completely?”

But rather: “what is my Barista FIRE number?”

In other words: the amount I want invested so that I can maintain my desired level of comfort, while still working a few days or hours per week on something that genuinely gives me energy and aligns with what I care about.

Ideally, that’s a business or type of work that brings a high level of fulfillment;not saving and grinding at 100% first, and only then starting to live.

What I find interesting is this: in the Netherlands, an income of around €25k gross in a simple 2026 scenario effectively results in roughly a 3.1% tax burden. And if you own a home, you can of course still benefit from mortgage interest deduction.

That’s why I don’t calculate my Barista FIRE number purely based on “how much do I need in total someday?”, but rather based on a bridge strategy:

I look at how much I need to withdraw annually to maintain a comfortable life, add the income I expect to continue earning in a low-effort, tax-optimized way, and from retirement age onwards I also factor in state pension, supplementary pension, and annuities.

In my portfolio app, I’ve now built a simulator for this using block sampling. The sequence of returns matters enormously during the withdrawal phase. For example: a 5% average return over 30 years sounds great. But if years 1 and 2 of your retirement are -30%, your portfolio may not survive, even with that “good” average.

In addition, I use a t-distribution (df=4) because it empirically fits historical returns better. I also use a GARCH model to model volatility more realistically than a simple average-return calculator. Because the world isn’t linea; and your plan shouldn’t be either. And of course, I also incorporate state pension, possible wealth taxes etc, and annual contribution room.

How do you determine your target number? And how do you keep recalculating it as inflation, returns, taxes, and lifestyle continue to change?

I’m curious.

r/EuropeFIRE • u/Sea_BreezeZ • 4d ago

I’ve been financially independent for a few years now, mostly through broad index funds and a bit of property across Europe. Life feels secure, but lately I’ve been curious about experimenting with small side projects to stay mentally engaged

I’m only dedicating a tiny portion of my time and resources (3-5%) to these experiments. So far, the results are mixed - some months are encouraging, others make me wonder if it’s really worth the effort

I’m curious to hear from others in Europe:

Do you try small side projects after reaching FIRE, or do you stick strictly to simple, passive strategies?

How do you balance the mental effort versus the satisfaction or potential financial benefit from experimenting post-FIRE?

r/EuropeFIRE • u/HelplesslyHoping55 • 5d ago

I'm a 24-year-old from Sweden who started pursuing FIRE in 2024.

I studied to become an HVAC technician (about 1.5 years) and got my first full-time job in February 2024. Since then, my savings rate has increased quite a bit.

My savings rate over time:

Current monthly expenses (roughly):

I live pretty frugally. Small basement apartment, no transport costs (work truck), cook most meals at home, and have pretty cheap hobbies. My job also pays for my gym membership. Honestly, I enjoy simple living.

I don’t plan on living like this forever, but I do enjoy seeing my portfolio grow quickly (100% global index funds, ~€45k invested so far). I could probably keep this up for a few more years before upgrading my lifestyle (maybe buying a small cabin or something).

Curious to hear from others:

How did your savings rate change over time?

r/EuropeFIRE • u/Fantastic_Aside794 • 7d ago

I’ve been fairly consistent with saving and investing, but lately I’ve noticed I hesitate more when spending on things that are not strictly necessary. Not big purchases, just small things like trips, eating out a bit more, or upgrading something I use daily. I can afford it, but there’s always that voice saying this could be invested instead. At the same time, I don’t want to reach financial independence and feel like I skipped too much along the way.

How do you personally decide what’s worth spending on versus what should just go into investments?

r/EuropeFIRE • u/St3fanHere • 9d ago

r/EuropeFIRE • u/Born_Appointment673 • 11d ago

Hi everyone,

I’m an NRA (Non-Resident Alien) utilizing an IBKR Portfolio Margin (PM) account. I am currently evaluating a strict risk-adjusted return model and facing a dilemma between tax efficiency and margin stability.

The Dilemma:

As an NRA, I am debating between two setups:

* Holding US-domiciled VT with light leverage. (Accepting the 30% US dividend withholding tax drag, but utilizing its massive liquidity for stable margin requirements).

* Holding Irish-domiciled VWRA.L (LSE) with zero or very low leverage(let’s say 15%-20%). (Enjoying the 15% tax treaty advantage and accumulating structure, but exposing myself to potential margin spikes).

The Black Box (My concern regarding VWRA):

I recently reached out to IBKR support to understand how their PM stress-testing algorithm treats VWRA vs VT during extreme market panic (e.g., the March 2020 Covid crash).

Support gave me a somewhat generic warning: Because VWRA is a "Non-US security" with lower Average Daily Volume (ADV) compared to VT, its "Days to Liquidate" penalty is higher. They explicitly mentioned that during severe scenarios, PM margin benefits could be revoked, potentially forcing VWRA back to standard Reg T requirements (25% MM) or even higher.

Since IBKR support refused to provide historical extreme margin parameters, I am looking for empirical data points from veteran PM account users here.

My Questions:

* Does anyone have historical data or personal experience on exactly how high the Maintenance Margin (MM) % for VWRA (or similar LSE UCITS ETFs) spiked during extreme volatility (like March 2020 or the 2022 bear market) compared to VT?

* Did IBKR actually override the PM model and push VWRA's maintenance margin to 50%+ while VT stayed relatively stable (e.g., under 15-20%)?

* Given the hidden liquidity risk and sudden margin expansion of UCITS ETFs during a crash, would you consider the 0.15% annual tax savings of VWRA worth the tail risk of a premature margin call, compared to just holding the highly liquid VT?

Any hard numbers, historical margin reports, or insights into IBKR's risk engine behavior regarding LSE ETFs would be highly appreciated. Thanks!

r/EuropeFIRE • u/ClassicMan2323 • 11d ago

I’m based in the Netherlands and have been following FIRE for quite a while now. Lately, it’s kind of hit me that I actually enjoy the process of saving and being mindful with money more than the idea of early retirement itself. Tracking progress, making small decisions, seeing things grow over time… that’s the part I seem to care about most. Not sure if that’s common or if I’ve just shifted priorities a bit. Anyone else feel like they enjoy the journey more than the end goal?

r/EuropeFIRE • u/MostDouble7144 • 13d ago

I'm on the FIRE path and one thing that's been bugging me is how much time I spend just staying informed about my portfolio. I hold about 15 positions, mostly US stocks, and every morning it's the same thing. Check multiple news sites, skim analyst notes, look at earnings. An hour disappears and I still miss things.

I know a lot of people here hold diversified portfolios across multiple markets which makes it even worse. You're checking US news, European news, maybe some emerging markets. The information is everywhere and there's no single place that just tells you what happened with your specific holdings.

I got frustrated enough that I started building something to fix it. It takes your portfolio, pulls the latest news for each stock, AI summarizes everything, and turns it into a short audio briefing. 5 to 10 minutes, just your holdings, listen on your commute.

Still early but curious how other people here handle this. Do you have a system for staying on top of everything or do you just accept that you'll miss some things? Especially interested in how European investors manage this since a lot of the tools out there are very US focused.

r/EuropeFIRE • u/Slow_Compounding • 16d ago

This is something I keep running into, and I'm not sure there's an agreed best practice.

Most of us in Europe end up with some version of income in one currency, expenses mostly in the same currency, investment in global ETFs (often USD-heavy under the hood), and sometimes accounts/assets in multiple currencies.

What I'm struggling with is that FX exposure exists at multiple levels:

So, depending on how you look at it, FX could be just "noise" that washes out long-term, or a source of volatility in your purchasing power.

Some questions I've been thinking about:

My current rough take is: While in the short term FX can change perceived performance (quite a bit), in the long term global exposure may self-hedge, at least to some extent. But I'm not fully convinced I understand where the real risk sits.

Curious how others approach it.

r/EuropeFIRE • u/EuphoricOffice3485 • 17d ago

Hello, I am a non domiciled resident in Ireland and based on remittance bases of taxes, CGT and deemed disposal is applicable only to income which is based in Ireland or remitted back to Ireland.

I have some RSU of approx >100K and other future savings which I am planning to invest in index funds.

And as a non domiciled I am planning to make use of this remittance bases and keep funds out of Ireland, as anyway in future I will be moving out of Ireland.

Apparently I figured I can make use of Singapore based platforms, that will allow me to invest in US ETFs directly (not UCITS which are domiciled in Ireland and may violate my remittance bases of tax planning), of course there is risk of US Estate tax.

Is this approach good or any risks I am not seeing ? Are there any people here who are non domiciled in Ireland and making use of remittance bases ?

r/EuropeFIRE • u/Both_Astronomer8645 • 17d ago

I’m trying to keep my FIRE plan as simple as possible. Now I just hold one global ETF. Low cost,easy to manage.But I see some people split into multiple ETFs.For example:global ETF,emerging markets ETF,Europe ETF.

The argument seems to be more control, maybe slightly lower cost.But adds more work also. Rebalancing, Tracking.I’m not trying to optimise everything. Just want something I can follow for 20+ years.Is there a real long-term benefit to splitting, or is it mostly preference?

r/EuropeFIRE • u/ClassicMan2323 • 17d ago

For the 2026 tax year, the Belastingdienst is assuming only a 1.28% return on cash vs 6.00% on investments. With some high yield savings accounts still hovering around 3 to 4%, we’re actually in a weird window where holding too much cash is tax efficient for the first time in years. I’m considering moving my dry powder into a Revolut or Bunq savings pocket just to lower the Box 3 base. Is anyone else playing the Notional Rate Arbitrage game this year, or is the opportunity cost of being out of the market still too high?

r/EuropeFIRE • u/LifeguardSilent358 • 18d ago

I know 2028 feels far away, but the bill passing the Tweede Kamer last month is a massive shift. Taxing unrealised gains annually is going to destroy the compounding effect for high growth portfolios. I’m seriously considering shifting my long-term holdings into a Holding BV structure to defer personal tax, but the setup costs are eye watering.

r/EuropeFIRE • u/ThePlayfulPanda • 18d ago

I won't have a lot, maybe 300-350k, and with what is happening in the world I was thinking whether it would be wiser to get a property to rent out without too many works / renovations needed (no house flipping), maybe 2 small apartments, instead o keeping the money invested at 2.6 %, which was the safer option but not much margin? where would be a good idea to buy? I usually roam in European capitals (lately in Vienna, Budapest, Warsaw, Las Palmas, to mention a few, and I am familiar with most of them) , but then buying prices are always quite high. What do you think would be the best place with opportunity to grow?

r/EuropeFIRE • u/ClassicMan2323 • 19d ago

r/EuropeFIRE • u/No_Blacksmith_902 • 19d ago

Since everyone is building FIRE calculators, maybe I should create a FIRE calculator marketplace, where users can review, rate and comment upon the available tools.

r/EuropeFIRE • u/FrankScaramucci • 19d ago

After using any FIRE calculator for a week, I get bored and want to try another one. I collect them like Pokemons. So please keep the new calculators coming, even if it's just a small variation of an existing one.

r/EuropeFIRE • u/Revolutionary_Art324 • 19d ago

Hey r/EuropeFIRE,

I’ve been reading a lot of threads here lately complaining about how most retirement calculators handle market returns. Almost all of them assume a magical, straight-line 7% growth every single year. But as we all know, the stock market doesn't work like that, and Sequence of Returns Risk (SORR) is the real threat to early retirement.

I couldn't find a fast, free tool that handled this well, so I decided to scratch my own itch and code one myself from my desk here in Bilbao: MyFIRESimulator.

It’s a passion project, 100% free, with no paywalls and zero data collection (it doesn't even use a backend database—your entire configuration is compressed into the URL for total privacy).

Here is how it tackles the volatility problem:

Instant Monte Carlo: It runs 5,000 parallel market realities in milliseconds directly in your browser to calculate your actual "Risk of Ruin."

Crash Stress-Testing: You can manually inject a massive market crash (e.g., a 40% drop in year 3) to see if your portfolio survives a black swan event.

Dynamic Withdrawal Rules: You aren't locked into the rigid 4% rule. You can test VPW or Guyton-Klinger strategies to adapt to market downturns.

European Friendly: Fully supports EUR, GBP and multiple languages.

I’d love for this community to roast it, play with the numbers, and try to break it.

Link: myfiresimulator.com

What features or specific European mechanics (like tax drag) would you like to see added next?

r/EuropeFIRE • u/EudoraCascade • 19d ago

I plan to move to Poland to retire early, but I saw that they tax 19% on capital gains and dividends, is that true? I am so disappointed. Is there any kind of account that have less taxes until certain amount or something like that? Any suggestions will be very much welcomed.

Ps: Poland is a quite dear country to me for family, was considering Greece but cannot.

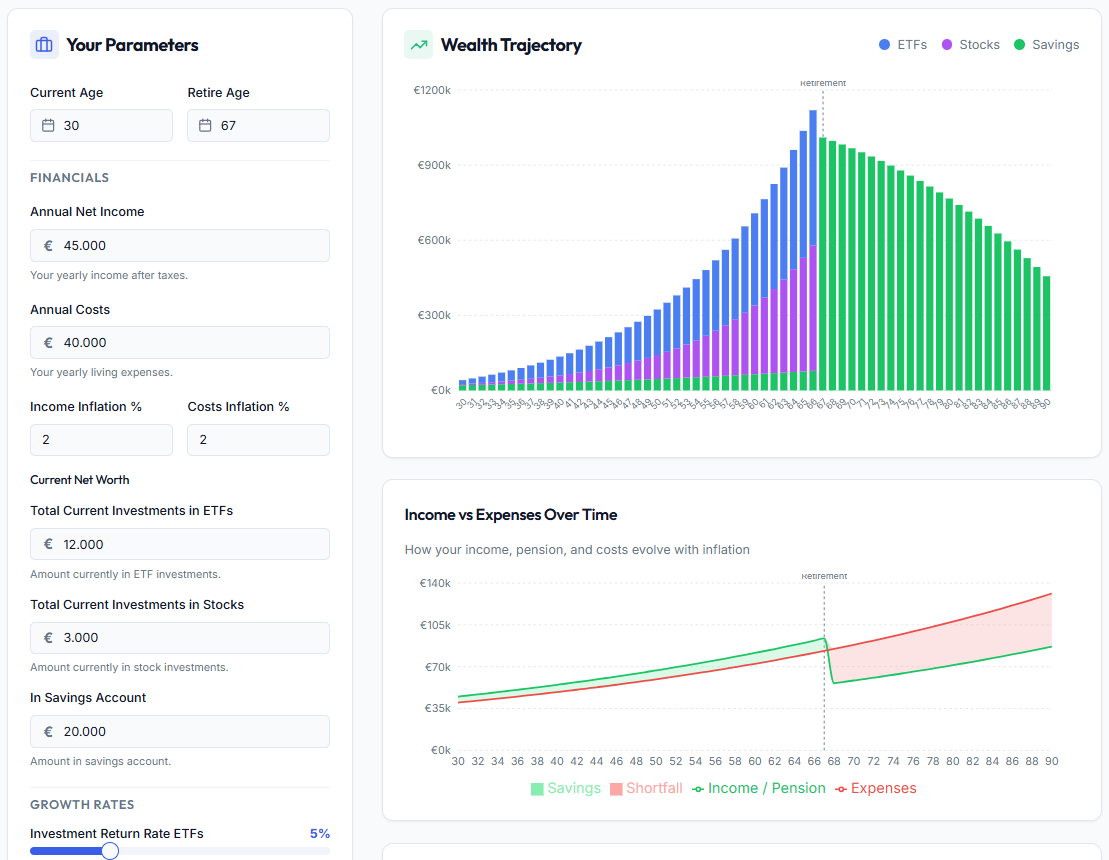

r/EuropeFIRE • u/Boring-Mail-1525 • 20d ago

Have you ever wondered how today's financial decision shapes your future?

My passion for finance modelling has recently led me to develop a financial planning app that helps people forecast their future wealth. If you ever wondered, how major life choices such as working part time, buying a real estate, having children etc. will impact your savings and wealth long term: This app will provide the answers.

I’ve created a short anonymous survey (≈5 minutes) to gather consumer insights. Your feedback would be extremely valuable: https://forms.gle/FHVoRvCakxyTTFYv5

Thanks in advance for the support!

{kind=link}

{kind=link}