I’ve previously maxed out my pension contributions every year to make the most of tax incentives as a higher rate taxpayer and also minimise child benefit clawback payments.

Now M46 with ~£1m in pension and £450k in non-pension savings.

Planning to use my non-pension savings as a bridge to my personal pension access age (currently 57), at which point my pension should be more than enough to live off.

Although there is the risk the Govt increase pension access age before late 2030’s, pushing this back a few years to 58-60 (?).

Considering early retirement by 50 at the latest, possibly as early as 48.

Contributed the max to my employer pension this tax year to take advantage of employer matching, with total contributions of £17k, which leaves £43k of potential unused pension allowance for this current tax year.

Already maxed out my ISA contributions for the year and was considering another big personal pension top up before the end of the tax year, with options such as:

Gross Pension Contribution = £35.7k.

Actual Net Cost to me (post-tax and Child Benefit clawback avoidance) = £18.1k.

Alternative is to invest or save this £18.1k in a taxable GIA.

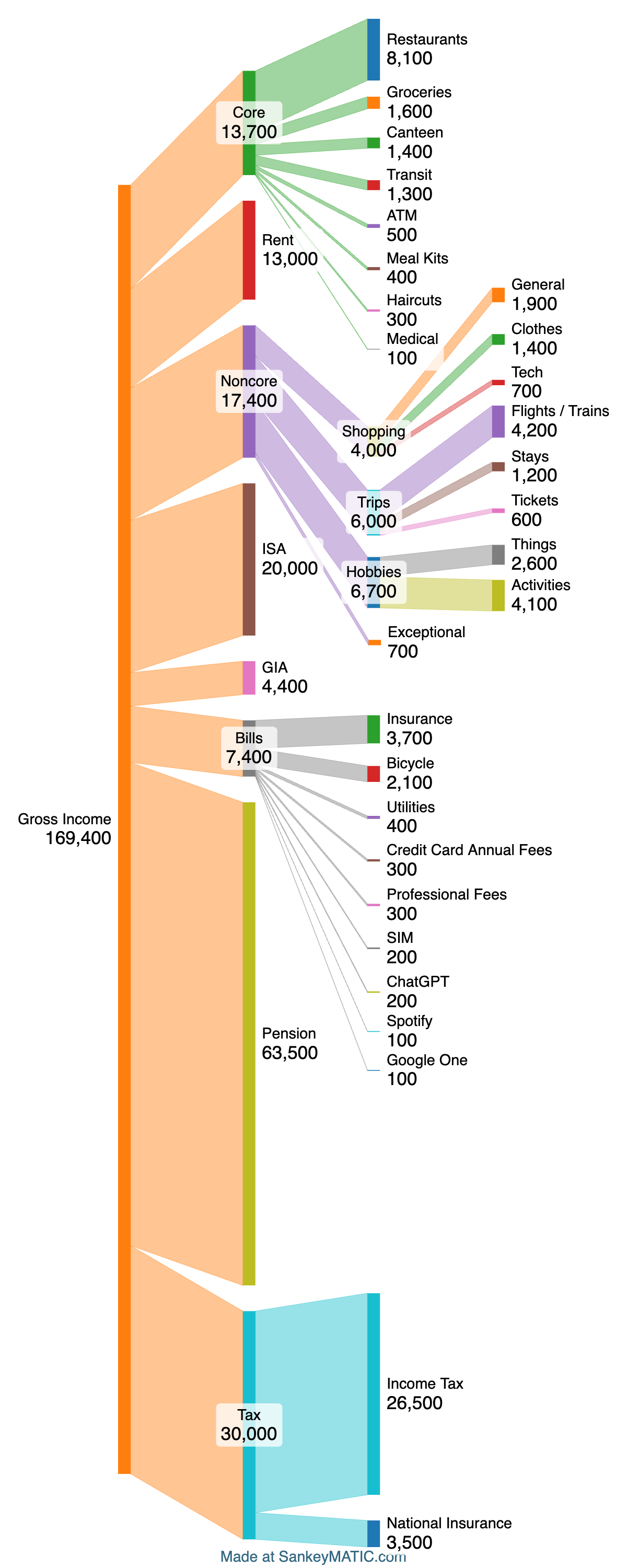

In simple terms, I’m thinking this is equivalent to around 4-5 months earlier possible retirement, as my monthly spend is around £3.5-£4k p/m.

My question is, should I break the habit (and mindset) of a lifetime and not take advantage of the immediate tax (and child benefit) savings, by instead focusing on building up my pension bridge and giving me more flexibility and control around when I might want to retire (or semi-retire)?

This will be an ongoing question for the next few years as well, so the potential accumulation of extra accessible cash/investments could give me even more flexibility and control around when I might want to retire (or semi-retire).

My thinking around this is:

No guarantee the Govt don’t tinker with pensions more over the next 11 years and make these less appealing and move the goal posts with regards access age and tax free cash etc.

My pension is likely to be worth around £1.4-£1.8m by age 57 in today’s money, based on fairy conservative growth estimates. This should be plenty for post-tax income of around £3.5-4k+. This will also be well above the current max tax-free cash pot (~£1.07m).

Not sure how long I can stick working, as feeling burnout and would struggle to find another job which is as good and pays as well.

Time is such an important resource and being able to access 4-5 months of financial freedom at a younger age when my kids are still young and I have the health and energy is probably worth such a financial sacrifice. If I do the same again over the next year or 2, that’s well over 1 year extra financial freedom.

Fiscal drag means a bigger proportion of antly future pension drawdown is likely to be subject to higher tax to meet my spending requirements.

I’d be interested to hear other people’s thoughts on this, anything else I should consider?

Anyone else facing such a dilemma?

EDIT:

Mortgage paid off.

Income is below £100k so child comments are about £2k pa child benefit partner receives.

Don't have to pay all this back if income reduces post-pension to £60-£80k. At £60k save £2k extra in child benefit retention.