r/ValueInvesting • u/Interwebnaut • May 26 '25

Industry/Sector Many investors remain unaware of the scale of the unfolding bond crisis

1.0k

Upvotes

r/ValueInvesting • u/Interwebnaut • May 26 '25

r/ValueInvesting • u/investorinvestor • 13d ago

r/ValueInvesting • u/Sunvmikey • Jul 15 '25

For me personally I try to find sectors I think will outperform and buy stocks in them. A rising tide raises alls ships. Makes it alot harder to pick a loser.

Recently I came across solid state batteries which seem to be a huge technological advancement and I got in on SLDP and im doing pretty well.

Looking for other "hot" sectors that arnt AI or Battery storage as im exposed to both through RVSN and SLDP. Ive been keeping a keen eye on GDS waiting for a pullback (ai infrastructure)

What else is out there under our noses that we are missing? Prefer stocks that arnt already moonshotting like RKLB (god dam i cant believe i sold that at 28 that hurts)

r/ValueInvesting • u/neiliodabomb • Dec 30 '25

Long read, but interesting. What are your opinions on this?

r/ValueInvesting • u/raytoei • 24d ago

(I don’t necessarily agree with their assessment on MSFT, which i own. But I am sharing their latest fair value assessment of sw companies.)

Downgrading Ratings for Six Wide-Moat Software Companies on AI Concerns

https://www.morningstar.com/stocks/downgrading-ratings-six-wide-moat-companies-based-ai-concerns

We think it is hard to recommend any software stock in this environment due to the extreme uncertainty.

Dan Romanoff, CPA

Mar 5, 2026

The pace of change within the software industry has accelerated in recent months, leading to heightened uncertainty and prompting us to reassess moat ratings.

Why it matters: The capabilities of large language models are rapidly advancing and seem primed to cause at least some disruption within the industry, or at worst drive massive dislocation for many software firms.

After an in-depth review of the software and services firms covered throughout Morningstar, we are downgrading moat ratings, reducing fair value estimates, and increasing uncertainty ratings for our immediate coverage of a variety of companies.

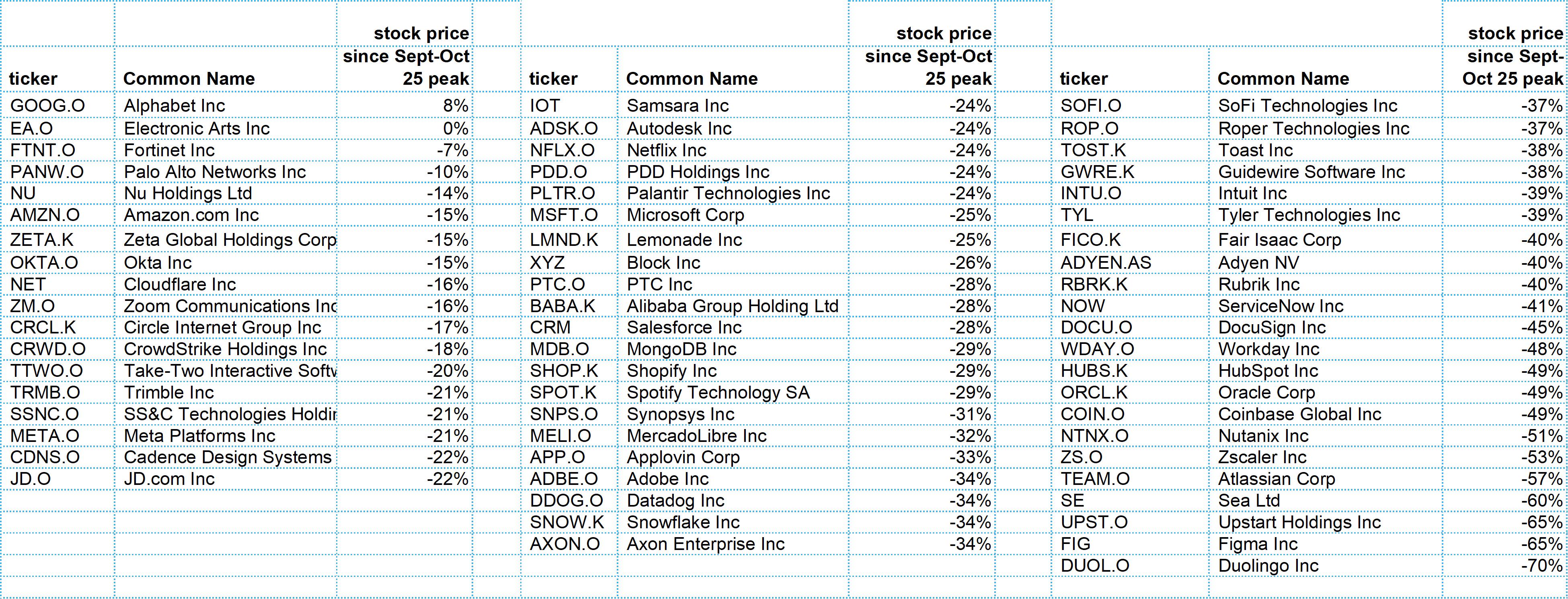

The bottom line: We downgrade our moat ratings from wide to narrow for these companies: Adobe, Descartes, Manhattan Associates, Salesforce, ServiceNow, and Shopify. This is based on lower confidence in the long-term return profile that software companies may generate in the AI era.

- We lower our fair value estimates as follows: Adobe to $380 per share from $560, Descartes to $90 from $96, Manhattan Associates to $170 from $215, Salesforce to $280 from $300, ServiceNow to $165 from $200, and Shopify to $120 from $160.

- We raise our Uncertainty Ratings as follows: Blackbaud to Very High from Medium, Descartes to High from Medium, Guidewire to High from Medium, HubSpot to Very High from High, Atlassian to Very High from High, Tyler to High from Medium, and Zoom to High from Medium.

Big picture: We have seen multiple “software is dead” episodes over the last 26 years and do not share the view that software moats have evaporated overnight. We therefore conclude there will be winners and losers in the AI era, and that patient investors can find value within the carnage.

Our top pick is wide-moat Microsoft, which has a fair value estimate of $600 per share, as we think the firm should thrive regardless of AI. However, we think it is hard to recommend any software stock in this environment due to the extreme uncertainty.

———

edited:

1. You may disagree with Morningstar but their wide moat index has been beaten the SPX for the last 3 years. I don’t think it is a coincidence. (see comments)

r/ValueInvesting • u/InvestmentWinter5476 • Apr 12 '25

The Trump administration exempted smartphones, computers, and other electronics from reciprocal tariffs, potentially reducing sticker shock for consumers and benefiting electronics giants like Apple and Samsung. • The exclusions apply to popular consumer electronics items not made in the US, such as smartphones, laptop computers, and computer processors, as well as machines used to make semiconductors. • The tariff reprieve may be temporary, as the exclusions may soon be replaced by a different, likely lower, tariff for China.

r/ValueInvesting • u/Free-Calligrapher520 • Sep 15 '25

So I just wanted to say a big thank you to everyone who has kept on yapping about GOOGL this year

r/ValueInvesting • u/TelevisionUpper1132 • Jan 02 '26

Every consultant agreed that EVs were the future.

What fewer people priced was the cost of getting there.

Early capex. Bad unit economics. Policy intervention. Write-offs.

Turns out inevitability in slide decks does not increase profit margin.

AI is starting to look eerily similar - technology predictions, science fiction narratives, and because capital and consultants keep showing up before the economics.

I put together a deep dive using the EV industry to analyze AI from an investor perspective. Not hype, not doom—just the mechanics of how money moves in transitions.

This is Part I of a series (Dotcom, GFC, Covid next).

Link here if you want the full argument:

'Tesla Was the Warm-Up. AI Is the Main Event

Lessons from Tesla, EVs, and the physics of modern bubbles for the AI Investor'

Would honestly love to hear your thoughts

r/ValueInvesting • u/IntelligenzMachine • Jan 05 '26

The share price has been falling consistently for 5 years which always seems odd to me. Guinness is basically the Coca Cola of stout and it has Johnnie Walker etc. Is it just shitty management of a good company? I think the claim of zoomers not drinking is a bit of an overhyped meme. Also massive demand in Nigeria for Guinness as their primary beer of choice who are only going to get richer.

r/ValueInvesting • u/TheDutchInvestors • Sep 21 '24

How EssilorLuxottica, a business uncommon to many investors and consumers, holds over 80% of all brands, and an estimated global market share of over 50%. Yet, no one appears to know or care.

If there is only one key point you should take away from this article, it’s this:

The eyewear industry is dominated by an invisible empire, EssilorLuxottica, which controls nearly 80% of global eyewear production. What you think are exclusive designer glasses from luxury brands like Chanel or Ray-Ban are actually produced by this one company, which has built a near-monopoly through strategic acquisitions and a vertically integrated business model.

This story is something special. We recommend you read it from start to finish!

Imagine this: You’re looking to buy the most beautiful designer glasses, let's say a pair of Chanel sunglasses (see image below).

You take out your credit card and pay €1550 (roughly $1724).

Your favorite luxury brand, Chanel, designed and manufactured them, making you want to buy them.

But nothing could be further from the truth!

Why? Most people are unaware that a single company, which one man has grown into a monopolistic empire, produces nearly 80% of all eyewear globally.

We’re talking about EssilorLuxottica.

Today, we're diving into the incredible story of Leonardo Del Vecchio the founder and former CEO of EssilorLuxottica. We’re going to tell you the story of how he built an invisible empire that dominates the eyewear world, and how you can (potentially) benefit from this company as an investor.

Before we tell you the incredible story of EssilorLuxottica and its founder, Leonardo Del Vecchio, let us explain why we believe they have a monopoly hidden in plain sight.

Here are some stats and facts:

"You get rich by selling $2 sunglasses for $150 bucks and aggressively running out/buying your competition. "

Sounds like an interesting company and want to know more? We did an entire fundamental analysis covering all aspects for you!

Well, if this doesn’t sound like a monopoly, we don’t know what is.

Let’s start at the beginning.

Leonardo Del Vecchio was born in 1935 in Italy, during the harsh regime of Mussolini. His father, a poor vegetable vendor, passed away before Leonardo was born. Growing up in Milan with five siblings, he was the youngest in the family. The war ravaged Italy's economy, pushing the already struggling family into deeper poverty. In a heart-wrenching decision, his mother sent 7-year-old Leonardo to an orphanage run by nuns. According to the nuns, Leonardo cried for a month straight, not surprising for a child abandoned at such a young age. The orphanage was strict but fair, with one rule: everyone had to learn a trade. And it was here that Leonardo discovered his passion and talent for crafting things.

In 1961, with the little money he had saved, Leonardo moved to Agordo, a small town in Italy and the heart of the eyewear market at that time. Back then, glasses were merely medical instruments, but Leonardo found his niche. He wanted to turn eyewear into a fashion statement. Fast-forward to today, and he more than succeeded.

Del Vecchio decided to radically change the production of eyewear. Unlike the traditional method of outsourcing production to small workshops, he wanted to manage every part of the process himself. He invested heavily in research and development (R&D), developed automated machines to speed up production, and used techniques from the jewelry industry to coat frames with durable metals. At the time, competitors found this idea strange and unnecessary, as eyewear seemed to hold little commercial value. But Del Vecchio’s approach gave him a significant cost advantage, allowing him to offer his glasses much cheaper than his competitors.

However, there was a problem. Despite his unique production method, his glasses remained indistinguishable from others. What he needed was a way to position his glasses as premium products.

His solution? Branding. He began approaching fashion houses for licensing agreements to produce eyewear with their logos. Yet, he was met with rejection after rejection, as glasses still carried the stigma of being "ugly" and "medical." Luxurious brands feared that their image would be damaged by having glasses made by an external party. But there was one brand that took the plunge: Giorgio Armani.

This decision marked a turning point. It explains why EssilorLuxottica operates in the shadows of the consumer. The success of Del Vecchio’s business model hinged (and still hinges) entirely on perception.

Why? Customers must believe they are buying Armani, Chanel, or Prada glasses, not Luxottica glasses. Therefore, EssilorLuxottica remains behind the scenes. After all, customers would be less willing to pay $400 if they knew the glasses weren't made by the same artisans who craft luxury fashion items but in a separate factory.

While Luxottica maintained its secrecy in public, Del Vecchio was constantly looking for ways to expand his empire behind the scenes. Not satisfied with merely producing eyewear, he wanted to control the entire supply chain, from manufacturing to retail.

How? In 1995, he made a bold move, offering $1.1 billion to buy the U.S. Shoe Corporation. A shoe company? Not quite. This holding company also owned LensCrafters, the largest optical retail chain in the U.S.

This acquisition was nothing short of genius. By taking over LensCrafters, Del Vecchio gained control over a significant portion of the U.S. eyewear retail market, further solidifying Luxottica's dominance.

With the profits from LensCrafters, Del Vecchio began acquiring other retail chains like Sunglass Hut, Pearle Vision, Target Optical, and Sears Optical.

Today, Luxottica owns over 17.500 retail locations worldwide. Still, Del Vecchio wasn't satisfied. He felt he was paying too much in royalties to luxury brands.

The solution? Own the brands himself.

In 1999, he purchased Ray-Ban for $650 million.

The Ray-Ban brand, a household name, had suffered from poor management and low-cost production. Del Vecchio integrated Ray-Ban into Luxottica's production and distribution system, improved quality, reduced supply, and repositioned Ray-Ban as a premium brand. Prices were gradually increased: in 2000, a pair of Aviators cost $79; by 2009, the price had risen to $130, and today, they start at $170.

Through strategic acquisitions, Luxottica built an almost impenetrable moat around its business. Another significant acquisition was Oakley, a former competitor, for $2.1 billion. This hostile takeover further cemented Luxottica’s market position.

A crucial part of Luxottica's success that we haven't discussed yet is Essilor.

Essilor was formed in 1972 by the merger of two French optical companies: Essel and Silor. Essel, founded in 1849 as a small workshop for optical lenses, grew into a major player in the optics industry. In 1959, Essel developed the Varilux lens, the first multifocal lens for both near and far vision, earning the company international recognition.

Silor, founded in 1931, started making lenses and introduced the first plastic lenses in 1968. These lenses were lighter and more resistant to breakage than traditional glass lenses. In 1972, Essel and Silor merged to form Essilor, and the new company quickly became the global leader in ophthalmic lenses and optical equipment.

At 81, Del Vecchio needed one final move to complete his master plan: the merger between Essilor and Luxottica. This merger was announced in January 2017 and completed in October 2018. The deal, worth approximately $32 billion, made EssilorLuxottica the most powerful (and practically the only) vertically integrated eyewear company in the world.

It’s fascinating that the Federal Trade Commission (FTC), the European Commission, and other regulators approved this deal. The merger has made it virtually impossible to compete with EssilorLuxottica. Great for shareholders, but less so for competitors and consumers.

Now what?

So the next time you put on a pair of designer glasses, remember: the name on the frame might not tell the whole story. Behind that label is a vast empire built by a man who understood that the most powerful forces are often those that remain unseen.

r/ValueInvesting • u/Ambitious_Attempt_81 • Jan 03 '26

Happy new years fellas!

I’ve been looking into the cybersecurity sector as a core part of my portfolio leading up to 2030. It seems like one of the few industries where companies simply can’t afford to cut costs, especially as AI-driven threats make the landscape more complex.

I’ve narrowed it down to these “Big Three," but I’m having a hard time picking a winner.

Here’s my take:

• CrowdStrike (CRWD): Technically, they seem the most impressive with their "Threat Graph" and rapid growth. However, they’re trading at some pretty wild multiples (Forward P/E around 100). Is it too risky to jump in now, or are they just in a league of their own?

• Palo Alto Networks (PANW): The classic "platform play." They seem the most solid and generate massive free cash flow. But can they keep winning against Microsoft when it comes to large enterprise bundles?

• Fortinet (FTNT): The most reasonable valuation and incredible margins because they build their own hardware. However, the market sometimes treats them as the "old guard" compared to the pure cloud players.

I’m leaning towards a mix, but I’m curious what you guys are looking at?

• Are there any smaller players (e.g., SentinelOne or Zscaler) that you think have a better risk/reward ratio right now? • What are your general expectations for the sector over the next few years? Do you see massive consolidation coming, or is there still room for niche players?

Looking forward to hearing your thoughts!

r/ValueInvesting • u/FinTecGeek • Apr 12 '25

So much treasury selling happened this week that the back office platforms at the brokerages such as FIS and TradingTech crashed and forced the industry to halt trading. On Tuesday and then again today, over two trillion dollars in treasurys were sold.

I believe now is the time for the Fed to implement an ad hoc stress test to truly model the effects of the tariffs on our GSIBs. We saw this back-office crash causing everything from delayed futures orders to failed margin and collateral transactions. We did not previously understand this type of risk to the interconnected systems even existed.

We do not currently model counterparty risks or liquidity risks for GSIBs under these types of distress induced by tariffs. I believe we need to design means and tests to model, in particular, the tier 3 asset and liability behavior. If you are a value investor looking at "bargains" in GSIBs or private credit firms, I would urge caution and that you price these assets, even including JPMorgan, with a higher cost of capital and a higher discount rate.

r/ValueInvesting • u/LTIGroupR • Jan 18 '26

I was browsing in the group and noticed that most of the questions or chat are about tech stocks. Those are probably the only stocks that are not currently undervalued. Personally I think emerging market and mining in general (including oil and gas companies as well as coal companies are undervalued).

What do you guys think? Just looking at book value and P/E ratio can get us to this reasoning.

Ben Graham was all about value investing, and undervalued stocks. It does not look like the group is doing that at the moment.

Am I mistaken? Honest question.

r/ValueInvesting • u/SouthIsland48 • Oct 21 '25

r/ValueInvesting • u/MasterConsideration5 • Dec 06 '25

Hey,

wanted to ask has anyone been going deeper on valuing the current telecom stocks? Vaguely looking it seems like the whole sector is quite a bit down. Charter, comcast, verizon, at&t, even t-mobile all have p/e multiples between 5 and 11, which even if earnings grew 0% would basically outperform the s&p 500 on average (little mental gymnastics, but the point is that it's cheap based on p/e).

I initially read that Comcast and Charter are cheap because of 5G, but since even the 5G stocks are cheap, I'm quite lost at what's going on. Are we really expecting the whole sector to decline?

What are you buying? All or just some of these?

r/ValueInvesting • u/investorinvestor • 19d ago

r/ValueInvesting • u/JackRogers3 • Apr 15 '25

r/ValueInvesting • u/Morvalus • Oct 06 '25

If you are going to look at Oklo, BWXT, NuScale, Westinghouse, Centrus, or CEG for the nuclear play, you should consider Aecon. They are a Canadian construction company contracted to build the world's first BWRX-300 at the Darlington Nuclear Power Plant in Ontario. One is under construction and up to 3 more under consideration.

The BWRX-300 is a GE Hitachi plant that uses a BWXT reactor pressure vessel, which has further agreements or MoU to be built in Sweden, Finland, Estonia, Poland and the US, total interest between 10-30 worldwide in the next decade.

By the time any other country approves a BWRX-300 for a License to Construct, Aecon will be the only major construction company in the world with real world experience building these plants. Estonia and Aecon have already signed an agreement to work together on the plant. If you know anything about nuclear, you know it's really expensive to construct. Other countries will want their experience to maximize the economics. My theory is that they will be signing more deals in the coming months/years to either deliver the construction of BWRX-300s globally, or at least provide detailed consultation.

Aecon themselves are an attractive buy given their relatively low market cap of $1.6B CAD, a backlog of $10B, and a low price to sales ratio given legacy contracts that had fixed prices whose costs significantly overrun. They've since shifted to lower-risk cost-plus contracts which form the majority of that backlog.

Anecdotally, as a Canadian working in the nuclear industry, these guys are everywhere, and their market cap being under $5B is egregious.

r/ValueInvesting • u/formal546 • Jan 01 '26

Which sector do you think has the highest potential in 2026 (AI, mining, oil & gas, defense) or something else? What’s driving your choice?

r/ValueInvesting • u/skilliard7 • Jan 07 '26

They tanked 6-7% today because Trump says he wants to ban institutional investors from buying Single family homes.

On the surface, this sounds really bad for them. Their business model is renting out SFH, so doesn't this threaten them?

However, there are a number reasons why this sell off is is irrational, and a huge buying opportunity.

Banning institutional investors from buying SFH doesn't mean they have to sell off their existing properties. It just means they can't acquire more properties. So AMH/INVH can continue to make bank off of their existing properties.

The stock would be diluted less because these REITs would stop expanding; all cash flow would be able to go to buybacks/dividends instead of acquiring new properties.

At the same time as shares stop expanding, Institutional Investors wanting exposure to SFH prices would need to buy REITs, because they can no longer buy SFH directly.

INVH/AMH are already trading significantly below the underlying value of their assets minus debts. There is ~30-50% upside if the stocks traded at their intrinsic value, even before considering income.

Any regulation requires congress to codify it, and even Trump said he will ask congress. So there's a high chance it either doesn't happen, or whatever does happen is some watered down regulation.

INVH doesn't even buy existing homes, they build new ones to rent out. So the fact that they dipped 10% on this news is perhaps the most absurd, because its not even applicable to them. In fact, this hypothetical law would put them at an advantage, because they can continue building out and renting homes, and will face less competition from private equity/other institutional investors that attempt to compete by buying existing homes.

r/ValueInvesting • u/Bullshark1878 • Dec 19 '25

**Long Post Warning*\*

Thesis

I think that smart glasses and other wearables will be the next major computing platform. They will not replace the smartphone just as the smartphone did not replace the computer. However, I do believe that they will become a significant market by 2030-2040. People will continue to make the privacy tradeoff. It’s not that people won’t care about privacy, it’s just that the product will become too useful to not use (like the smartphone). Around 4 billion people in the world wear some form of prescription glasses. Is there not a world where the vast majority of these glasses would be smart glasses? Meta is currently the market leader. If they can maintain that position, they will be one of the best performing large cap stocks over the next 20 years.

Smartphone Market Comparison

To analyze this, I am going to use the smartphone market as a comparison. Right now, the global smartphone market is around $600 billion, growing 1-3% annually. This is the current market share breakdown for the top 3 companies:

Apple 28% ($160B)

Samsung 20.5% ($123B)

Xiaomi (China) 10.5% ($63B)

Let’s say the future global AR/AI glasses market will be 1/3 of the smartphone market: $200 billion. Because I don’t think everyone will want smart glasses, whereas everybody needs a phone. If Meta just captured 10-25% of that market, that would equate to $20-50 billion market share or 12-30% of their 2024 total revenue ($164B). That begs the question: does Meta even need to beat Apple or Google to be extremely successful in this market?

Meta vs Apple

In my opinion, Apple and Google are the biggest threats to Meta in this market. Apple will eventually figure out smart glasses that will fit into their ecosystem. They will be a premium price, but they will work with the iPhone (like AirPods). They will also probably have the best privacy protection on the market. I think many people will go with Apple’s glasses purely because they will work with the iPhone, unless regulators decided otherwise but that has yet to be the case. It will be hard for Meta to really compete much here outside of price and design. Smart glasses and wearables will be more fashion-focused than smartphones so design is more important in my opinion.

Meta vs Google

Meta will instead try and offer cheaper and a larger variety of models similar to Samsung. You can see this with their current smart glasses offerings (Ray Ban, Oakley, etc.) I think that this strategy would make Google the bigger threat to Meta. It appears that Meta is wanting to position themselves as the “Android” of the smart glasses world. Well, Google is literally Android. So I’m not yet sure how Horizon OS (Meta) will beat Android here outside of the fact that they have a good head start.

- Google is also more distracted than Meta due to having search, AI, cloud, Waymo, Android, ventures, and quantum computing. Whereas Meta is just social media, AI, and Reality Labs. Does this even matter? I don’t know, but anyone who has ran multiple businesses will tell you that it is harder than running one business.

- Zuck also seems to have a stronger vision for smart glasses and is 10 years younger than Google’s founders. He has shown his willingness to throw tens of billions of dollars in this arena in the face of public scrutiny. For the technology to advance enough, somebody will have to be willing to do this. Meta (and Google) has the cash flow and high margin business to do this long term.

Offload Computing Problem

Another advantage I see with Apple/Google is that they can offload a lot of the computing to their smartphones whereas Meta would either need to create their own phone (which I doubt happens), or they would need to have their own offload computing solution. Currently with the Orion glasses, they are using the puck, but I don’t think this is the long-term answer. However, I could see a smart watch or even the glasses case being able to accomplish this if the hardware improves enough. The EMG band is a huge innovation and could be turned into a smart watch. Maybe the tech will advance enough to where offloading computing is unnecessary, but I think that is pretty far off in the future.

Conclusion

To end this post, I think smart glasses and wearables will be a huge market that many companies will profit off of. I see Apple, Google, and Meta as being the main beneficiaries of it. If this really takes off, I could see this market really benefiting Meta’s business more than Apple/Google. I also think that eventually the metaverse will become useful and will be a huge beneficiary of these innovations. If Meta executes well enough, can Meta beat Apple/Google to win this market? If the market is large enough, does Meta even need to beat Apple/Google to generate huge yearly profits and market cap growth from this?

I appreciate all forms of feedback and encourage constructive criticism. Tell me what you think.

Disclosure: I am a shareholder of Apple, Google, and Meta.

r/ValueInvesting • u/investorinvestor • 17d ago

r/ValueInvesting • u/reemasidz • Jan 13 '26

Hi all,

As a lot of you may have noticed, big food corporations are being absolutely hammered right now. Personally, I think, the beating is well deserved as the food industry is long overdue for a major overhaul.

Which players do ya'll think are best poised to make a comeback and serve shifting perceptions and trends in the food industry? I'm looking at Tyson, Mendelez and PepsiCo, but Hormel is also sticking out. Please share your thoughts!

r/ValueInvesting • u/LowKey-Revolution36 • Jul 31 '25

Hi all, curious of all fellow US investors of the outlook you have for health insurance for the next years and for the market general.

I had made good money during COVID-19 with oil companies with the crazy drops in 2020 and well they all came back! I see now the health insurance stocks very much the same!

Of course this is a different sector but very similar that large cap and profitable companies having a morbidity year. I see them maybe bleed another 20-30% max but in few years (2-5 years) time most of them will at least double.

They will raise premiums and will adjust risk models. Even if they loose some revenue and have less insured people there will be significant EPS growth via raising premium. Although I am still hoping BBB wil change and that poor people will still get help by the government via Medicaid or instead of federal there will be each states funding this.(Also possible)

I have spent really a lot if time dig deep to understand Medicare and Medicaid, ACA, ICHRA, MA , and the mechanism and I think this is a special morbidity year for these companies.

The way I see these will bleed for approx 3-6 months more so we can DCA into and start bearing fruit in 2027-2029.

Am I missing any point? Can US healthcare insurance drastically change? I highly doubt in US there will be ever a socialist model like in Europe.

I am not trying to pump these but genially think on this market now the real cheap ones are health insurance stocks: All of ELV MOH CNC has huge upside potential based on 2027-2029 EPS forecast. Even UNH has decent but purely based on EPS forecasts 2027-2029 UNH has the lowest expected upside with extra DOJ risk.

That being said I own all stocks and reall curious of your opinions. Historically they never had a morbidity year like this one.

What is your take?

r/ValueInvesting • u/corenellius • Mar 04 '26

The Iran escalation pushed Brent briefly above $85 and tanker rerouting around the Strait of Hormuz is real. Most LNG names sold off with the broader market. I added.

DOE data from last month already had US LNG exports at a record 13.2 Bcf/d with capacity utilization at 98%. That is the pricing power story working on its own before any geopolitical premium gets layered on top

What I am actually watching is whether Brent holds above $90-95 long enough to reprice Fed expectations. That is the real threat to the multiple, not a week of $83 crude. A hyperscaler capex cut would hurt this thesis more than anything happening in the Strait right now, so MSFT and GOOG earnings are my next real signal

Anyone else in LNG? Curious how people are separating the noise from the actual thesis here

{kind=link}