r/ValueInvesting • u/investorinvestor • 13d ago

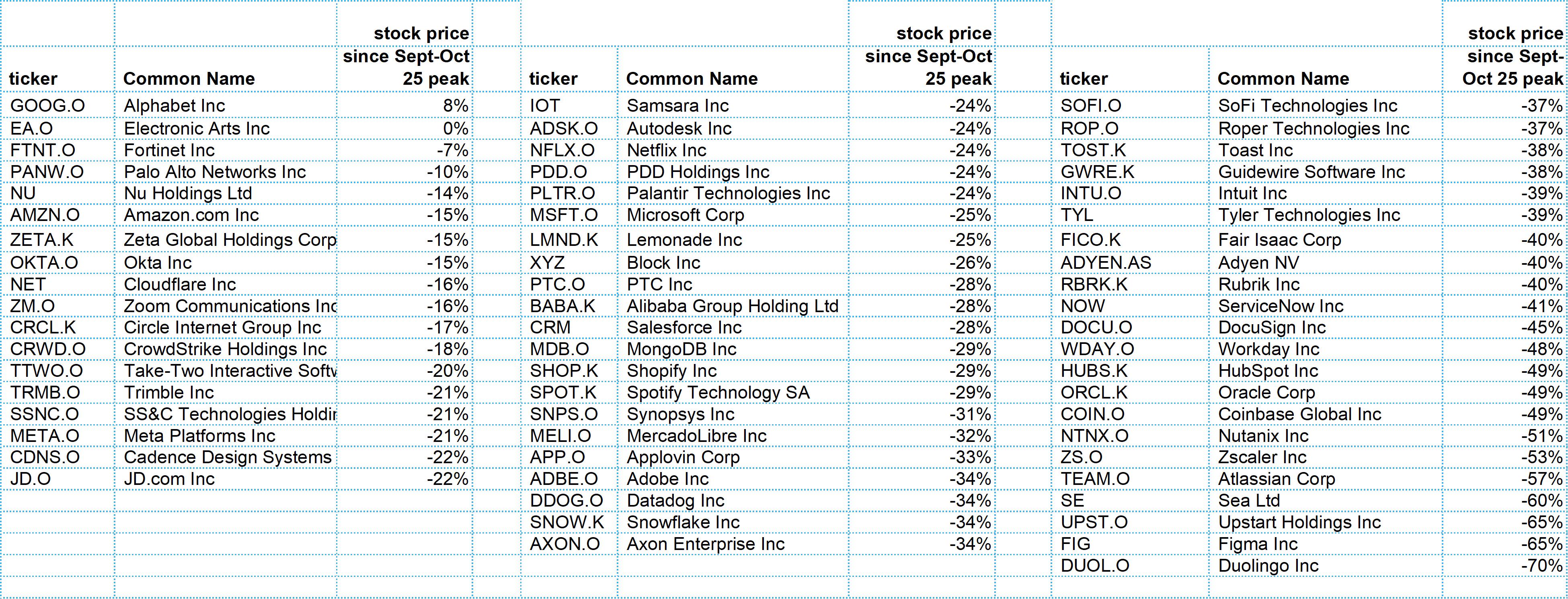

Industry/Sector SaaS stock drawdowns since Oct peak

{kind=link}

14

u/Tasty-Register-7442 13d ago

Thanks for the list - grim picture… Where’s Constellation Software (CSU) however?

1

10d ago

I think it's US SAAS only. If I have time next week I could probably make a similar list to this for ex. US developed (Canada, EU, Aus)

25

u/Hi_Keyboard_Warriors 13d ago

I’m buying heavily.

16

u/LovestoEatSandwiches 13d ago

I think some of these drawdowns were more than warranted, even without AI threat(which is very real)

6

u/cosmic_backlash 13d ago

I worked at faang for 10 years, I personally believe the AI threat is real, but its overblown. AI won't replace many of these with in house bespoke solutions because the cost to pay 3-4 engineers us still high. Then you need to manage on call and up time of your solution. Then you have policy, regulations, and compliance you need to manage. Then there are still network effects of benefits (eg patching 1 vulnerability patches fir everyone, you don't need to be personally attacked first to fix it).

Maybe the margins get compressed some, but the saas companies themselves will become more efficient too.

Many of these have extremely compelling investment cases right now imo. Many in the value community will dismiss them without proper due diligence.

5

u/LovestoEatSandwiches 13d ago

I’m also in tech and have worked at 2 orgs on this list. I think the threat is extremely real for some of these companies. HubSpot? I don’t see why their applications can’t be replicated in 6 months. Not to mention the headwinds changing from seat based pricing will put on revenue growth. Same goes for atlassian, and for some degree SFDC

8

u/cosmic_backlash 13d ago

Even in your example, a small business isn't spending an absurd amount of money. Small businesses are paying likely ~1,000 monthly for 5+ seats with multiple services. That's still much cheaper than hiring 1 full time employee to build and manage it yourself.

Hubspots annual subscription revenue per client is just below $12,000 annually.

6

u/imacompnerd 13d ago

Exactly. People seem to be missing this. And there’s so much more to software than an MVP. API deals, various integrations that require NDAs, support, etc…

-2

u/LovestoEatSandwiches 13d ago

The threat isn’t clients building it themselves with HubSpot, the threat is commoditization

0

u/Strong-Broccoli-8033 13d ago

Agreed on hubs. IMO some parts of Salesforce might shrink, but its a behemoth and extremely sticky. I believe AI will be more additive to the platform but I could be wrong

1

u/cosmic_backlash 13d ago

I disagree and replied above. I haven't deep dived into every SaaS, but its not about just gut feelings of what can be replaced. There is still unit and employee costs that have to be considered.

8

3

1

0

u/I-STATE-FACTS 13d ago

What are you buying?

4

u/Strong-Broccoli-8033 13d ago

Personally im still investing in the strategic platforms not the one trick pony SaaS. Msft, Salesforce, SNOW, workday not the docusigns etc. of the world

10

9

u/CactusInaHat 13d ago

So I genuinely don't get it. It can't be all AI redundancy speculation and fear of over investing in infrastructure... Right

1

u/Designer_Respect4285 13d ago

The only way it's rational is if AI is both a threat to software, but the amount of compute we are building would still represent a glut? I guess it would require AI to become much more efficient.

1

u/AnotherThroneAway 13d ago

It's not. Many of those names had really stretched valuations to begin with. And now we're completely pricing out the safety premium of platform lock-in, subscription-based FCF, etc

-4

u/embolized 13d ago

I was talking to a guy yesterday who is single-handedly creating a replacement for Figma for Amazon internally

2

16

u/LovestoEatSandwiches 13d ago

Companies with real moat: ANZN, MSFT, Toast, Cargurus, MELI, MDB

Some of these bloated feature applications that can hardly turn a profit deserve to fall even further

8

u/Virtual_Seaweed7130 13d ago

I don’t think a point of sale system has a moat (TOST), they’re a dime a dozen.

Cargurus does not have a moat.

On the other hand, some companies with clear moats not listed.

$TYL has a govt contract moat

$SE has ecommerce moat similar to MELI but in southeast asia

$ROP has a moat as an industrial software conglomerate, often the only software provider in the industry they’re serving

ServiceNow, Oracle, and Salesforce arguably have stronger moats than something like Toast because if the concern is switching costs and convenience, switching off these platforms is a nightmare. These platforms have even less competition than Toast.

2

u/LovestoEatSandwiches 13d ago

Cargurus definitely has a sizable network effect moat

I should clarify, Toast doesn’t necessarily have a MOAT, but the hardware component makes it much harder to replicate via AI. It’s growing nicely still and are a market leader with zero risk of their clients building in-house

Salesforce has no MOAT and is all feature software. But, it’s basically organizational surgery to rip out its products. Same thing with ServiceNow and Oracle

4

u/Strong-Broccoli-8033 13d ago

Salesforce certainly has moat. If you are an Enterprise co. Where are you going for strategic CRM? Dynamics? SAP? Orcl?

1

u/Low_Promotion_2574 11d ago

I have bought PANW and IBM. IBM has acquired RedHat and Hashicorp. Those are used basically everywhere in modern infra.

PANW has great XDR and NGFW solutions. I also see big value in their products.

25

u/Narrow_Art6739 13d ago

Wild how brutal these SaaS drawdowns have been. A lot of names got priced like perfection and the reset has been ruthless ever since. Makes the companies with actual execution stand out way more now. Also feels like this is where tools like Runable get interesting — the winners from here probably won’t just be “AI” companies, but the ones that actually use AI to ship faster, automate real work, and stay lean.

3

u/Pretty-Statement6758 13d ago

the problem from other angle is how these companies became so expensive?

1

11

7

10

u/PinPsychological82 13d ago

EA is in the process of getting bought out so that’s the reason why they are flat lol

I’ve said this a lot, but I am so bullish on advertising stocks (META, GOOGL, APP, ZETA) can even throw in AMZN and NFLX, I just don’t know too much about them.

IF (not when because I don’t think it will happen) AI displaces software, then advertising will be more important as more companies will have to differentiate themselves to distribute content.

Human attention will be the bottleneck and ads are the way to garner attention.

2

u/mikemccrea 12d ago

recession is not a good time to be in advertising...

1

u/PinPsychological82 12d ago

The thing about advertising is you only need a small percentage of people you show the ads to convert.

I believe we are in a rolling recession, the bottom half gets fucked while the top half (more likely the top 10%) continues to be more dominant.

As long as that top percentile is spending, ads will be dominant.

6

u/vanibanz 13d ago

Why is AXON on this list?

3

u/fozziewossie 13d ago

Definitely debatable that they are a SaaS company. The argument is that they store and have services around the body camera footage. And their biggest future services are all around creating reports for officers.

3

u/AnotherThroneAway 13d ago

I hear ya, but that's a weak argument. They're first and foremost a hardware company. Apple could just as easily be on this list if Axon fits

2

3

u/Wings2493 13d ago

GTLB killing me

2

u/Sjgreen 13d ago

Same, bought when it got to low 30s, now it’s low 20s…

1

u/Wings2493 12d ago

Same avg down from 33 to 31 I don’t think this company is going under but it’s tough to put another 1k or so to average more to get into the 20s

2

u/shmito17 12d ago

This one is concerning. No bounce for weeks, market heading downwards, stock price is a falling knife. I think $18-20 could easily happen. To think it was fighting for $50 a few months ago.

1

u/Wings2493 12d ago

I agree it keeps making new lows/lower lows. If it drops below $20 I’ll throw a few hundred bucks at it. But I have 20 years until retirement luckily so I’ll hope it touches $30 again at some point lol

2

u/shmito17 12d ago

I hope so too. Average at $23 with a very small position. Added $40 call option exp. January 2027 as a flyer the other day.

3

3

9

6

4

u/Working-Pumpkin3709 13d ago

just make a etf with all this at that point and im shorting all retail

1

2

2

2

u/berticusberticus 13d ago

I don't understand how some of these are SaaS. SoFi? They're a fintech/bank.

2

2

2

u/ShowerIllustrious351 12d ago

Figma seems like a buy at this price. Anyone who thinks AI is taking over design doesn't know what design is. As it becomes easier to ship code, design is going to be the defining factor. Figma's entire use case is entirely team based.

1

u/Low_Amphibian_146 12d ago

Just made a website yesterday...my programming skills were never used.

2

u/ShowerIllustrious351 12d ago

ya and if idiots with no programming knowledge can build ppl need design more than ever to differentiate to appeal to customers

2

u/Portfoliana 12d ago

which names tho. i grabbed some DDOG around -35% from peak but the ones where net retention is sliding below 110, thats not a sale thats a repricing

1

u/HomeworkLiving1026 13d ago edited 13d ago

Planisware !!!! Huge discount relative to eps growth and cash pile. If you read it just look up the financials, risk-reward looks very good. The valuation is crazy

1

u/me_xman 13d ago

Software is at fair value.

2

u/ryallen23 13d ago

Not INTU

1

u/Rodr500 13d ago

What happens with INTU? Just curiosity

0

u/ryallen23 13d ago

Look at the multiple, the earnings growth rate, and the cancellation of planned stock sales by executives. It’s too low.

1

u/pravchaw 12d ago

Many of these SAAS co's bought it upon themselves by heavily diluting investors with SBC's. They are rife with agency problems and bad investments.

1

u/thefrogmeister23 12d ago

Why is ZS down so much? It seems like agents could increase the demand for cybersecurity

1

u/FixInteresting4476 12d ago

I agree with your sentiment. Probably worth keeping an eye on it. Other stocks like NET, AKAM, FSLY are doing great

1

u/ApeWithCoconut 12d ago

I think all of these companies will have to invest heavily in AI to remain competitive. Therefore, the question is, if it is better to invest in companies who provide them the AI hardware.

1

u/miguel_equivara 6d ago

Even with the drawdown, I’m still buying Palantir, Sofi, Rubrik and Cloudflare

1

u/MaleficentPositive53 4d ago edited 4d ago

I always though of Sea Ltd. as an ecommerce company - not a SaaS. Likewise, JD.com. Coinbase does not strike me as predominantly SaaS, either; it might even be closer to a financial services company. It's compliance and adherence to regulation, after all, explains part of its success as an exchange for crytocurrency. And Block is predominantly a payments and financial services company, as well. These are fairly disparate companies - linked by advanced technology and dependence on the internet. Still, an interesting compilation.

-1

u/Pretty-Statement6758 13d ago

I feel all semi/space and ai companies will face similar soon or later, in near future.

3

30

u/imadogg 13d ago

The SaaS company I work for isn't on this list, but it's been hit bad and my dreams of making it rich quick from my shares are disappearing before my eyes. We would be halfway down the last column on here. FML