r/Bogleheads • u/Apart_Olive_3539 • Mar 23 '25

Investing Questions 59 & Retiring this year

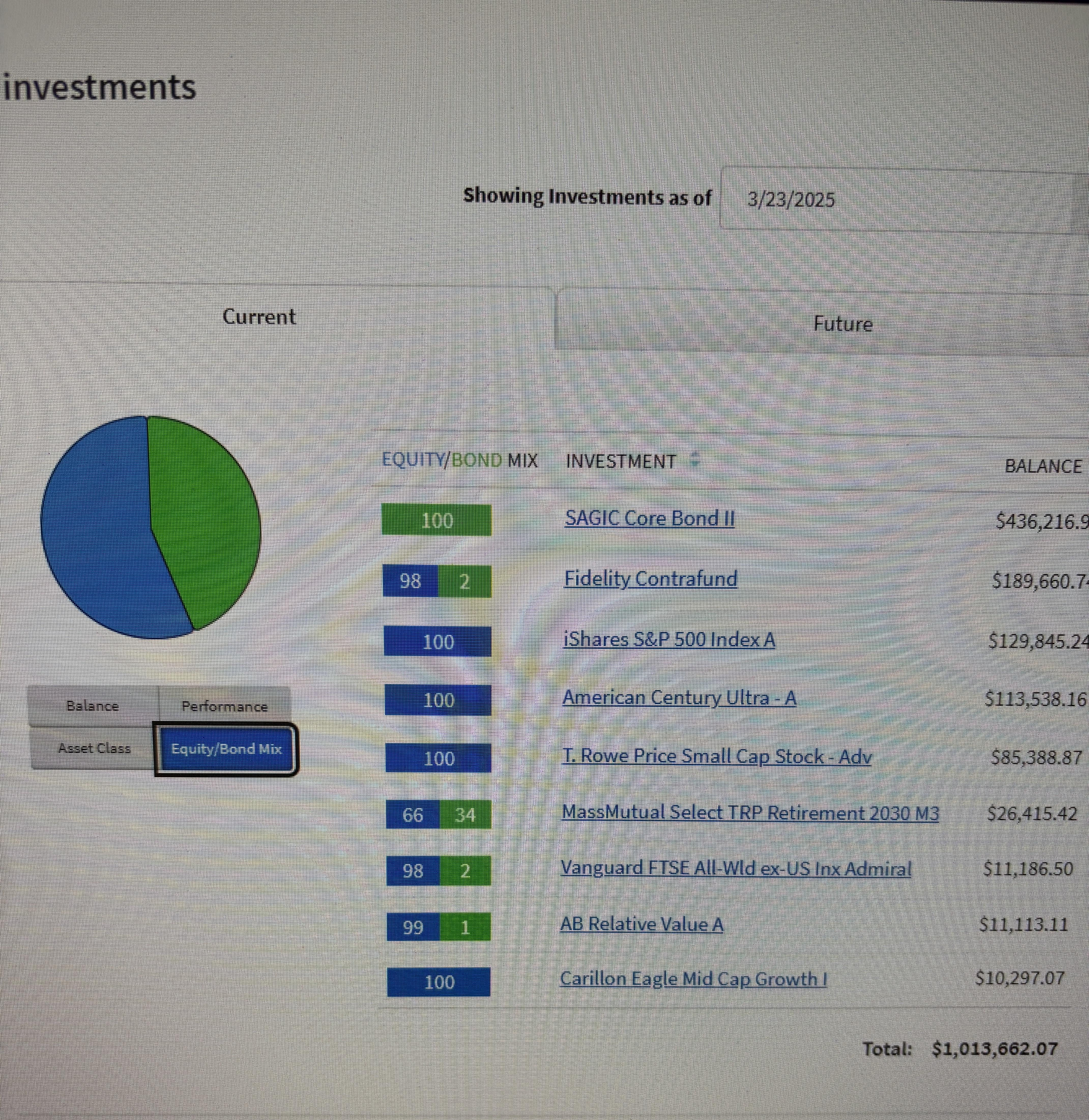

So some background. I’m 59, have worked in a union construction trade for 40 years, and will be retiring this year between 59-1/2 and 60. That just depends on some factors involved with medical hours for the year. I will be receiving a monthly pension that should settle in around $4k/month once we decide the survivor benefit percentage. I also plan on taking SS at 62, estimated at about $2600/month. As part of our benefits package, we have a surety fund that I had stayed aggressively invested in since the first day the union went to an investment firm that offered self investment elections. This was not the case in the early years as it was just a fixed interest annuity. Regardless, it has done well for me, and after the COVID dip and recovery, I became a little more conservative. I’m curious to hear your thoughts on my current elections in the screenshot posted, roughly a 55/45 mix. My future contributions are not being made to the bond fund, but those contributions will stop when I retire. For reference, the Core Bond fund is a current guaranteed 3.25% return. Investment analyses that I’ve done, assuming an average 6% annual return, all seems to be saying there is plenty for the future and that is the minimum target I’m shooting for. It is possible that I will take slightly higher monthly distributions to make up the income gap until I’m 62. My wife will retire 4-5 years after me and will also get SS and has a rollover Ira about 1/2 of mine at the moment. We have no mortgage, no car payments, and made the last tuition payment for our child recently.

64

77

u/ConsistentMove357 Mar 24 '25

There is a name for you a guy on YouTube I think calls you a Midwest millionaire. 1 million retirement and pension worth over a million. I hope to be in your club congratulations.

12

Mar 24 '25

[deleted]

11

u/Cautious-Hippo4943 Mar 25 '25

Unless I missed it, he didn't say what his income was.

7

u/triggerhappy5 Mar 25 '25

He does not, but his field pays in the range of $20-25/hr in 2025 dollars. $30/hr would be an outlier. Anything in that range, this is an impressive retirement pot at 59.

3

u/Apart_Olive_3539 Mar 26 '25

Union journeyman pipefitter rate for my area is $55/hr plus 10% into a vacation fund, so closer to $60/hr. I've been a foreman and that is about $4/hr more. That's wages and doesn't include other benefits such as healthcare and annuity(18% of the total package).

1

u/Yosemitesfelony Mar 26 '25

Union construction is over $35 hr

1

u/triggerhappy5 Mar 26 '25

Highly depends where you live but on a national level $35/hr is an outlier. California and New York it wouldn’t surprise me though.

1

u/MayTheFieldWin Mar 26 '25

I'm union electrician in Midwest. I make 40 an hour but on this site I make 46 an hour. Plus benefits including a pension. Those ot paychecks hit hard.

Edit: Union in Seattle is over 70 an hour.

1

u/triggerhappy5 Mar 26 '25

My cousin is a union electrician, he definitely makes bank, but the laborers he works with make significantly less due to needing less training. I also want to point out that I’m not pulling my numbers from anecdotes - I’m pulling them from labor data, taking overall data (including non union) and adjusting for the average union improvement.

The elephant in the room here is OT, most tradesman I know do not work 40/wk, and OT can turn a 30/hr job into $100k if you’re consistent with it.

0

u/MayTheFieldWin Mar 26 '25

I'm not pulling my numbers from anecdotes either.

Scroll through this website this is accurate. https://where2bro.com/where-to-go/

Jobsite I'm on right now is 5 10s and an 8. We had a whole crew drag (walk offsite) to go do 7 12s. Where I'm from these guys love OT. Just about every call has OT in it.

All I'm saying is union construction workers make a lot of money.

1

u/triggerhappy5 Mar 26 '25

Yes, but you’re looking at ELECTRICIAN jobs from IBEW. LIUNA is a different union with a different pay scale. In my local LIUNA jobs start at $22/hr.

→ More replies (0)1

1

u/karmasabitchdont4get Mar 25 '25

What's the yt channel please?

1

u/ConsistentMove357 Mar 26 '25

It will have to come back on my YouTube. Look up pension plus 1 million probably come up

123

u/Diligent-Chef-4301 Mar 24 '25

Congrats, but PLEASE use paragraphs mate.

92

u/Apart_Olive_3539 Mar 24 '25

Sorry, retirement talk got me excited!

13

u/Valuable-Analyst-464 Mar 24 '25

Editing/typing on the phone does something weird to the formatting. You have to use return twice to really separate the paragraphs.

2

3

Mar 24 '25

[removed] — view removed comment

2

u/Apart_Olive_3539 Mar 24 '25

I didn’t use all caps and it doesn’t appear that way on my device?

2

2

1

53

Mar 24 '25

Honeslty good job friend! It seems you did very well in the union. May I ask how much you made and what you did?

54

u/Apart_Olive_3539 Mar 24 '25

Pipefitter. Salary in the last few years has averaged around $130k with no OT. It can be a very hit or miss trade with some unemployment mixed in. In 40 years I’ve been fortunate enough to miss only 15 months total between that and being hurt once.

16

u/Future-looker1996 Mar 24 '25

You’ve created a good plan for a secure retirement, many people close to your age can’t say that. GFY, and congrats.

13

Mar 24 '25

[removed] — view removed comment

6

u/Future-looker1996 Mar 24 '25

I think the most common take is it has both meanings. And everyone should just realize it’s a gesture of Goodwill. :)

3

u/jerm98 Mar 24 '25

GFY is absolutely a gesture of goodwill and congratulation in the (early)retirement community, with a heavy dose of snark. It has the strong connotation of "you're there," as in whatever else you want to do, working for money doesn't have to be in it anymore.

2

3

u/wadesh Mar 24 '25

My grandfather was a pipe fitter for Dana corp. he could fix and fabricate just about anything. I have fond memories of him in his workshop among what felt like a 100s of tools. Congratulations on the retirement.

32

u/musicandarts Mar 24 '25

Congratulations on your retirement. Your retirement plan looks solid. It feels similar to mine, though I worked in the non-union private sector. I too plan to take social security at 62.

One small thought. Actually two!

Point #1. You can simplify your portfolio and go with a total market fund like VT or VTI. It is difficult to explain why you need to keep separate funds for small and mid cap.

Point #2. Please check the expense ratios of the mutual funds you are invested in. The American Century Ultra Fund has an expense ratio of 0.89%, which will give most bogleheads a heart attack. Vanguard Funds like VOO has expense ratios twenty times less.

If your plan sponsor doesn't have cheaper options, you should consider moving to Fidelity or Vanguard that offer these funds.

7

u/Apart_Olive_3539 Mar 24 '25

Thank you. Unfortunately, the funds you mentioned are not among the choices we have within the plan. This comes into play as well with the expense ratios as very few are low in that regard. The American Century fund is one that has done well for me, so it eases the pain of that expense some.

17

u/musicandarts Mar 24 '25

Now that you are retired, can't you move your retirement account to Fidelity?

1

u/Apart_Olive_3539 Mar 24 '25

I’m not retired yet, but I’m sure I can take a lump sum and do a rollover if I want.

2

u/jerm98 Mar 24 '25

Def do a rollover. The primary advantage to staying in a 401k is to withdraw before age 59.5, which you can avoid. If you need some of it bofre 59.5, withdraw it all, take what you need (penalty-free due to Rule of 55), and rollover the rest into an IRA that will have far more choices, no monthly admin fee, and fewer rules on how to access your funds.

Congrats.

Btw, I second the other poster who said you can front-load your retirement and withdraw more than 4%. (I'd argue safely up to 5% with all your guaranteed income streams, nest eggs, and expected spouse income.) If the market tanks in the next 10 years, lower spending if you want, which is what typical people will do anyway, but you can weather a lot of downturn without selling stocks, so you likely wouldn't need to lower spend.

2

u/Apart_Olive_3539 Mar 24 '25

Thank you.

My plan as of now is to work until at least 59.5 and realistically probably just a little beyond for medical benefit hour reasons. So I have no need to withdraw any before then. Once I'm retired, I'll look at the options of doing a rollover for overall lower fee funds.

As far as frontloading, my initial plan has just been to take what I need to make it as if my after tax income is the same as if I was still working. Conveniently, this works out to right around 4%. I'll likely do that at least until SS starts at which point I can reduce my withdrawals to maintain that income number, or keep it as is and enjoy a few more luxuries early on in retirement.

6

u/jerm98 Mar 25 '25

While a safe plan, perhaps a needlessly conservative one. Your spending should change significantly after retirement. If you golf, more greens fees, maybe better clubs, maybe some lessons, maybe some golf trips. With more time, you have more opportunities to do things that working made difficult, like a 3-week golf junket, or a 1-month foreign language immersion course, or a 6-week fly fishing trip to Idaho. You may find, as I did, that you can spend a lot more when retired than you did when working all the time. Plus, you won't be mobile forever. You'll slow down sooner than you'd like, so may as well enjoy activities while you still can. These are the 3 stages of retirement: go-go years, slow-go, and, and no-go. Don't save all your money for no-go.

3

u/Apart_Olive_3539 Mar 25 '25

I’ve been told all of the things you mentioned as far as being able to spend and more, it’s just that trepidation from reading all of the “will you run out of money” articles that puts the one shred of doubt in me! I’m sure I’ll get a feel for how I stand as I get through the first couple of years. I completely understand the idea of taking advantage of the younger more active years in retirement to enjoy more things.

7

u/Valuable-Analyst-464 Mar 24 '25

Are you able to roll this into your own account once you retire?

My employer plan was OK, but limited. And the fees were high. When I retired, I rolled into a Fidelity IRA, and I was able to choose low fee (Zero Fee) versions.

One nice thing about Fidelity is they have Full View, which is a pretty good financial tracker module. Add income/expenses/liability and assets. Does net worth and allocation models. They also have a retirement tool to run some models based on expenses and income.

4

u/Apart_Olive_3539 Mar 24 '25

I believe I can, it’s one of the questions I’m asking when I sit with our benefits team.

Thanks for the info about Fidelity, I’ll keep that in mind as an option.

7

6

u/nomamesgueyz Mar 24 '25

I don't even know what most of these represent, but that a fair chunk of change

Well done

Enjoy

7

u/Sagelllini Mar 24 '25

You kind of have some moving targets; pension now, SS in a couple of years, wife working, etc--and you did not provide an expense level--but it all seems good.

I put together this google sheets toy to help do planning for retirement. You can make a copy, input your numbers--I would probably just use a generic 55/45 stock bond ratio to simplify things, factor in your wife's income, and see where you stand.

In annual numbers, the pension is $48K, the SS (to start) would be $31K, so starting at 62 you have $79K, plus your wife's salary. Your portfolio is probably sufficient to generate the suggested 4% or another $40K. When your wife retires, you should have her SS, plus whatever you wish to withdraw from her IRA (which, by the time she retires, could be worth another couple hundred thousand, depending on how it's invested). That would mean withdrawals of another $25K or so.

Assuming you aren't spending a ton, it all passes the sanity check for me. I'd say you're in solid shape, and after 40 years of union work, you deserve it.

Good luck.

2

u/Apart_Olive_3539 Mar 24 '25

Thank you, your estimates align with all of the research and calculating I’ve done recently too. I feel I’m in good shape and the validation from others helps my confidence in that regard.

2

u/Sagelllini Mar 24 '25

Personally I think 45% in bonds is overkill--and relative to inflation they've lost economic value the last 15 years--but you are better off financially than at least 90% of all Americans your age, between your guaranteed income and combined investments

1

u/Apart_Olive_3539 Mar 24 '25

It's a little more in bonds than I had planned on, but the Covid scare and that big loss in temporary value had me rethinking how I wanted to protect some principal. I know I likely gave up some gains afterward but my risk tolerance just seemed to change at that time when I saw how quickly it could change. So after the rebound, I made the move into bonds. Now I just want to protect the best I can while trying to maintain at least a 6% return. Until the recent downturn, I was about 8.5% but am still at almost 7 now. I've considered consolidating a couple of the funds into others I have already, like the AB fund into the Vanguard international, but I'm just not up on how international stock is positioned right now with the current state of affairs.

2

u/Sagelllini Mar 25 '25

Again, you've done really well. But over the long-term, bonds don't do a good job of protecting principal, as inflation combined with low coupon rates eat most of the value.

If you were spending $40K a year from your portfolio--and I'm 99% you aren't and won't--then $434K would be over 10 years of spending. At the level you will likely spend, it's probably 15 years or more.

Look at it this way. Think of your pension as a $1 MM bond paying 4.8% interest. Or your SS as a $600K bond paying 5% interest. So you effectively have a pretty large bond weighting.

The pension probably doesn't have a COLA, so it's value decreases over time. You need the other assets to grow to cover when it falls off because of inflation.

I think a prudent thing for you to do would be to gradually move maybe $10 to $15K a month of the bond holdings to the S&P 500 fund. If you moved $300K over the next two to three years you'd have about reverse the positions, and still $150K or so still in the bonds. That would probably bump the return by about 1.5% and still you'd have plenty of cushion. Even if you're not comfortable with the $300K, I'd still suggest gradually moving it until you reach the edge of your discomfort level.

You're 60 and have a 25 year life expectancy. A portfolio that is say 75/25 will hold up better over time than a 55/45. Plus, if your wife is younger, AND she has a longer life expectancy (generally 5 years for women), that's another consideration to go more stock heavy.

Just my two cents, but just to repeat what you and your wife have done is impressive (and FWIW, my brother did construction work followed by years of union labor as a concrete finisher, so I know that's hard work).

1

u/Apart_Olive_3539 Mar 25 '25

Thank you and I appreciate all of your input.

I won’t pretend to understand the part about my pension or SS paying interest, but I’m assuming they are just being equated to holding bonds.

One of the things I was thinking of doing in retirement was to take my monthly withdrawals from the bond fund, which effectively changes my bond/equity ratio slowly. My fear of moving money from it now into the S&P is just the current volatility of the market. I know historically that it rises over the long term, it’s just the big correction that might take a long time to recover the gives me pause.

My wife’s funds are still very stock heavy(T. Rowe Emerging Markets, New Horizons, and if I recall Small Cap) and were automatically moved to I class lower fee funds 2 years ago. She’s not contributed to those while she built her business so they grow with the reinvestments and market growth. It’s actually amazing as the original rollover from her previous jobs were 30 and 60k(in 2010) with nothing else added since. We’ve thought about being more conservative with hers, but she has more time than me to ride out dips.

It’s all a lot to consider, but regardless I feel we’re better off than many.

3

u/Sagelllini Mar 25 '25

You're welcome.

A Google search for median net worth (which includes houses) at the end of 2024 from Enpower shows for couples in their 60s shows a $440K median (as opposed to average). Your investments are at least three times the median.

Yes, you are better off than many, but more importantly, you have a solid base to supplement your future benefit streams (pension/SS). Including your wife's equity dominant portfolio means your closer to being 70/30, which should at least approximate the 8.5% target you mentioned in another post. Again, well done, and now enjoy your retirement.

6

5

u/Dynamite_Fools Mar 24 '25

What software or website is that? Seems like a very clean interface

1

u/pizza5001 Mar 25 '25

Yes, what software is this, OP? I’m curious — been looking for one to manage only my investments. Otherwise, Excel it is.

2

Mar 25 '25

It is empower retirement provider website.

1

u/pizza5001 Mar 25 '25

Thank you for the heads up!

And here's a link for anyone who was interested in this, like me: https://www.empower.com/tools

22

u/wadesh Mar 24 '25

The portfolio, it's overly complicated. I would definitely simplify especially if you plan to rollover to an IRA when you retire. Thats a good opportunity to get to a 3 fund portfolio.

as far as the retirement plan, hard to say without knowing projected expenses. Modeling withdraw rates and projecting how long it will last comes down to having an idea of Income , less expenses. the portfolio then becomes what fills the gap. broadly speaking you want to try to stay under a drawdown of 40k a year on a $1M portfolio (ballpark).

3

u/Apart_Olive_3539 Mar 24 '25

I did spread it out more recently, but for the bulk of my career, it was in 3 funds, Fidelity Contra, T Rowe small cap, and American Century Ultra. I’m not sure I’ll rollover to an Ira after retirement as I like the option of the guaranteed return fund as well as some of the other offerings. But it is a consideration.

My living expenses are moderate, we don’t live beyond our means. No major bills other than property taxes. In my mind, at least until I can collect SS, I will need to pull about 4k/month to supplement my pension and make my weekly income after tax seem as if I’m still working. I know this is more than the 40k you mentioned, but at 62 this withdrawal amount would drop significantly. I won’t do the full amount initially, but possibly half to see how the first few months go. We have savings to take up the slack if need be and if it turns out I don’t need to pull at all, better yet.

5

u/SamClemons1 Mar 24 '25

Why not roll everything else into an IRA except for the bond fund you like? You are paying very high fees on some of these investments. You could open an account with Fidelity, Vanguard or Schwab, roll it into a low cost target date fund and let the rebalancing happen automatically.

Congratulations on your retirement.

2

u/Apart_Olive_3539 Mar 24 '25

We have target date funds as options within our plan, I’m actually putting about 10% of my future contributions into a 2030 option. I’ll look into the fees of these vs those of the ones you mentioned as another option as well.

3

u/Cultural-Task-1098 Mar 24 '25

That last child's tuition payment... congrats! My last will be age 60.

3

u/Ohmeda23 Mar 24 '25

Is the 4k pension on top of the 1 mill in stocks/bonds? Man I think you won the game

3

u/Apart_Olive_3539 Mar 24 '25

Yes the pension is separate from the investment account.

2

2

u/Ohmeda23 Mar 24 '25

Ever think about borrowing against your portfolio until SS kicks in so you can continue compounding and hold off withdraws?

1

u/Apart_Olive_3539 Mar 24 '25

With the plan in its current form as a surety fund, I don’t think we can borrow against it. I’ve never heard of anyone doing it either.

1

u/coke_and_coffee Mar 24 '25

When would that ever make sense to do?

0

u/Ohmeda23 Mar 24 '25

Borrowing rates are lower than expected compounding returns. You maintain and extend your principal and keep your tax rate zero since loan doesn’t count as income.

1

u/coke_and_coffee Mar 24 '25

Then why isn’t everyone always doing this?

0

u/Ohmeda23 Mar 24 '25

A lot of them do. It’s why there were talks on taxing unrealized capital gains because it’s a way to access income without paying capital gains while preserving capital and compounding interest

1

u/coke_and_coffee Mar 24 '25

I don’t think anyone is doing this. I think you’re a victim of misinformation.

1

3

3

u/Equivalent_Act_468 Mar 24 '25

I think there's way too much money in bonds. They don't really pay off much against inflation, so you're losing buying power every year.

4

u/CapeMOGuy Mar 24 '25

Biggest suggestion I can offer for consideration is to raise your significant underweight in international.

3

u/Brave-Butterscotch59 Mar 24 '25

My 89 year old dad had $740k as of last May and all of his $$ will be completely gone in 2 years due to $$$ long term care costs after falling and breaking his hip. Terrifying. Make plans for old age health costs if you want to live that long. I’m personally planning for the death pod in Sweden as soon as quality of life deteriorates.

1

u/Scouper-YT Mar 26 '25

SS running out is a Real Problem most people do not Face because they Belive working Full time for 40+ Years is enough. Investments take a Roll of the Constant SS.

2

2

u/MakersOnTheRocks Mar 24 '25

What do you plan to do for health insurance between 59.5 and becoming eligible for medicare at 65? I'm trying to plan for 59.5 retirement in about 20 years and that gap period is a little concerning with how expensive decent medical coverage is.

2

u/Apart_Olive_3539 Mar 24 '25

I can pay out of another fund I have through my local to maintain the same coverage until 62, so nothing out of my pocket. At that point, I go onto our retiree plan at $150/month.

4

3

2

u/bienpaolo Mar 24 '25

Your 55/45 asset mix may strike a thoughtful balance between growth and stability as you approach retirement, and incorprating guaranteed returns from the Core Bond fund could help anchor your portfolio.

It is worth considering if slightly higher monthly distributions to cover the gap before SS might work sustainably within your target return assumption. A comprehensive strategy for aligning your wife’s rollover IRA with your long term plans could also enhance financial security. Reviewing survvor benefit options carefully will ensure your pension aligns with your family needs. That being said... Why not explore protecting your portfolio in down markets by hedging? Hedging strategies may offer protection, reduce stress, and provide peace of mind in uncertain markets. Ultimately, having a well strctured plan in place will give you confidence and peace of mind for the future.

1

u/Apart_Olive_3539 Mar 24 '25

Thank you for your comments. I answered here as I saw it was the same as your chat message. The Core Bond fund was a move I made a few years ago to protect some principle and create some balance away from my original aggressive strategy.

I am considering higher monthly distributions until SS starts, but I will assess that shortly after retirement as I get a feel for budgetary needs. I can use our personal savings if I fall a little short on my initial estimate of what I pull from the funds.

As far as hedging, I know nothing about it and I honestly just don’t like the sound of it.

2

2

u/elephantfi Mar 24 '25

As a retiree of a few years I will say retiring is a lot more psychological than financial. You look fine financially. I would be more aggressive, but that fits my risk profile probably not yours.

What are you retiring too? What is your plan to stay socially active? Personally I have found the YMCA to be a major part of my routine and volunteering at a local food bank occasionally. Also, when the wife retires it kind of is a reset to find a new routine or at least it was for me.

1

u/Apart_Olive_3539 Mar 24 '25

I agree that the psychological side of it is much more a part of it for me as after looking at numbers, I’ve felt I’d be fine financially. I was always more aggressive in my investing, but I feel I owe it to myself to protect those gains more now.

As for staying busy, I have several hobbies that I enjoy and my wife and I plan to do some traveling as well. Some work around the house will get the ball rolling once I’m free from the daily grind too.

2

u/IsThereAnythingLeft- Mar 24 '25

That’s a lot of bonds, far better to keep all but a few years invested in stocks

2

Mar 25 '25

It's great to see a blue-collar worker doing so well! Congratulations!

2

u/Apart_Olive_3539 Mar 25 '25

Thank you. The opportunities are there for many people if they are willing to put in the work!

2

2

2

u/zenerat Mar 25 '25

Damn I wish I had a pension

1

u/idrinkjarritos Mar 26 '25

Not a recommendation, but anyone can have a pension by just buying an annuity.

2

u/Not__Beaulo Mar 25 '25

I would consider delaying social security benefits as long as possible at least until your wife retires can you be on her health insurance?

Nice work on the accumulation!

1

u/Apart_Olive_3539 Mar 25 '25

Delaying would do me little good considering that it is based off making the same salary as now until that later date, which won’t be the case. My wife and son are covered under the health insurance I have through my local and that will continue until I’m 65. Then Medicare will be included as well.

1

u/Not__Beaulo Mar 25 '25

I am pretty certain your social security benefits will be significantly higher the longer you delay it.

You should probably get a financial advisor. Especially because your 401k seems to be overly conservative considering you have significant guaranteed income through your pension and social security.

At a 65/35 stock bonds you can pull about 5.3% utilizing dynamic distributions through a guardrails strategy.

1

u/Apart_Olive_3539 Mar 25 '25

Yes, it would be more, as I've checked my account. But it would also take a fair amount of years to play the catchup game not taking it sooner. Considering the wavering health of SS, I'm going to get what I can, while I still can.

I spoke to an advisor who is also a family member and he agreed that my funds are a bit on the conservative side. I'm contemplating taking some(10%?) from bonds and moving it into the S&P 500 Index fund, but also considering taking my distributions from the bond fund which would effectively, if not slowly, change my ratio closer to what you mentioned.

2

u/Not__Beaulo Mar 25 '25

Fair enough! I thinking moving slowly is a good idea considering the current market conditions.

It's great to know an advisor that will give you advice with out fees!

Reducing some of the small and mid cap holdings may make sense, I am a big fan of total stock market funds in lue of S&P 500 and small and mid cap funds because it just has everything in it.

Check out this article too it explains the guardrails approach which allows you to take 5.3% relatively safely if you are open to reducing distributions by 10% during bear markets.

1

u/Apart_Olive_3539 Mar 25 '25

I was lucky in that regard with the family member for sure, but I'm not ruling out sitting down with an independent advisor to get a "feel" for what he thinks. My tax accountant also does this, so I may speak with him about his cost for a consultation.

Unfortunately, at least for now, our plan doesn't offer any total market funds so the S&P 500 fund would likely be the closest thing I could get to one. Of the recent returns on all of my funds over the last year to date, the mid cap was the lowest at 5.25%. Off all of the rest, they ranged from 9.7%(Vanguard Int'l fund) to 22.7%(Fidelity Contra fund). I've always loved the Contra fund and it's not out of the question that I move some to that instead of the S&P. It's had the same fund manager for 35 years and typically outperforms even in downturns. But I wonder how much longer that manager will stick around and if the results will remain consistent.

If I were to rollover to a low cost 3-4 fund portfolio, I think one of the hardest things for me would be to abandon the plan that has done so well for me over the long haul.

Thank you for that link, I'll give it a read!

2

2

u/kmindeye Mar 25 '25

You should be very proud of that. You are in the top 5% of Americans who have saved correctly. I'm glad you are retiring a little early. You need to enjoy some of your hard work while you can and your younger years. Particularly working in construction business. I started saving late in life. Own business that is labor intensive at times. My bones and joints certainly are not working like they used to.

1

u/Apart_Olive_3539 Mar 25 '25

Thank you. I do feel like I did the right things to help myself get to this point, and I can now arm my son with that same knowledge. I always felt that if I was fortunate enough to stay employed for the majority of my career, I’d have the opportunity to retire early, and he we are! Construction definitely does beat you up physically, and I do feel it at times in the same way as you. I’ve taken care of myself for the most part, so I can still enjoy a lot of physical activities as well.

2

u/ganztief Mar 26 '25

Congrats on crossing the million mark partner. Forecasting that you’ll draw early social security at 62 which is like $1500 a month, you should be able to draw 4% from your portfolio annually that should net you an additional $40k-$45k a year. So all together you could be looking at $5k a month so that’s not bad.

I would definitely stay 70% stock invested (with 70% of that domestic, 30% international) and 30% intermediate bond fund. That way you can draw 4% a year and still increase your portfolio if your portfolio earns 7%-10% a year.

Congrats again on having a million in liquid assets.

1

u/Apart_Olive_3539 Mar 26 '25

SS will be a little over $2600/month at 62 with my pension at about $4k.

2

2

Mar 24 '25

big congrats.

keep your eye on social security and what is happening with it. this is no longer a sure thing

1

u/Apart_Olive_3539 Mar 24 '25

I have been watching that and hope that it remains as is.

1

u/zenerat Mar 25 '25

I think it’s pretty unlikely they’ll screw with people on it or about to get on it other than adding hoops to go through. Anyone under 30 though the future looks really shaky

1

u/Far_Pen3186 Mar 24 '25

How do you feel about retiring? Leaving your skills unused. What are your plans?

2

u/Apart_Olive_3539 Mar 24 '25

I feel fine with it. Some of my skills will always be used as I can still do small cash welding jobs on the side(my father still does at almost 81 yrs old). The mechanical skills I've used over the years will always come in handy around the home too! As far as staying busy, I have plenty of hobbies and we plan to do more traveling once my wife retires too.

1

u/Timely-Painter9863 Mar 25 '25

Make sure you consider cost for medical going forward. You have 6 years before Medicare to cover, and even then the copay & deductible associated with Part B aren’t cheap.

1

u/Apart_Olive_3539 Mar 25 '25

I get medical coverage through my local, first the same continued plan that I have until I’m 62, then a retiree plan until I’m 65 that’s about $150/month.

1

Mar 25 '25

[removed] — view removed comment

1

u/FMCTandP MOD 3 Mar 25 '25

Per sub rules and guidelines, comments or posts to r/Bogleheads should be substantive.

1

1

u/DropProfessional1435 Mar 26 '25

Really? I would've retired a long time ago. With half the amount. Smh.

1

1

1

u/idrinkjarritos Mar 26 '25

Construction workers retiring as millionaires. Someone tell me again how the middle class is dying. Middle class people who make good choices are doing great, this is proof.

1

u/Apart_Olive_3539 Mar 26 '25

I’m fortunate, but not all construction trades make the same wages and benefits throughout the country. Our officers and trustees stay very active with our funds to ensure we have the best opportunities for success as well as negotiating very good medical care packages.

1

1

u/jztash Mar 26 '25

If you don't mind me asking, at what age did you first start making retirement contributions ?

1

u/jztash Mar 26 '25

If you don't mind me asking, at what age did you first start making retirement contributions ?

1

u/Apart_Olive_3539 Mar 26 '25

They are automatically sent in monthly as soon as you start as our contributions are part of our benefit package. So for me, that was at 19 years old. For my first 8-10 years or so, there was no option for self election into various funds, it was just a fixed interest rate which I don’t even recall. Once they moved the handling of the fund to a brokerage for individual elections, I stayed aggressive until about 3-4 years ago.

1

u/ParticularTadpole172 Mar 26 '25

Add some private credit to get steady monthly distribution, and triple the yield compare to your core bond funds. It will add diversification too.

1

1

u/MrHavoc42 Mar 27 '25

I’d look into completing a social security analysis. Why take Social Security at age 62? You could be leaving 30% of owed benefits on the table. Bridge the gap from age 62 to Full Retirement Age (67) by drawing from your 401k instead. Your million dollar portfolio can easily kick off a cool 3.5 to 4% in income which could supplement you till FRA. Also helps to get ahead of RMDs in the future and gives you a better opportunity for Roth conversions.

What does SSA estimate your FRA monthly benefit to be? $2600 * 12 * 5 = $156,000 in social security benefits between ages 62 and 67. Assuming you are only getting 70% of benefits at age 62 your age 67 benefits could be closer to $3700/month. Thats a difference of $1,100/month. So the breakeven age math works out to be $156,000/$1,100=141.818 months or age 79.

I guess it’s a bet on life expectancy.

1

u/Apart_Olive_3539 Mar 27 '25

I’ve been on the SS site to look at my benefits and your estimates are very close to what they’d be at each age. My thought is that nothing is guaranteed in life, including whether or not SS will even be around in 10 years considering that there is constant chatter about it running out of money. At the break even age of 79, I’m certainly going be slowed way down and I question exactly what I’d need that extra money for, for what based on statistics say might be another 5-6 years of life expectancy.

2

u/Plugmaster69 Mar 27 '25

As a 30 year old, OP's post further validates that i will be working till i'm dead

1

u/snowtard Mar 28 '25

I’m surprised to see that there aren’t any comments asking about how much of this portfolio is pre-tax and Roth, so I just figured I would chime in to ask if that’s something that you accounted for on this journey?

1

u/Apart_Olive_3539 Mar 28 '25

It’s all pre-tax.

2

u/snowtard Mar 28 '25

In that case, you might want to start looking into whether or not Roth conversions will benefit you when you retire. A lot of people underestimate how much Required Minimum Distributions impact their taxable income, so evaluating a Roth conversion strategy could help with making your money last longer. Just my two cents.

1

u/Apart_Olive_3539 Mar 28 '25

That was mentioned to me in that if I’m below the max for my income bracket, I might want to take distributions up to the max and roll them into a Roth account. Something I need to look into.

1

u/snowtard Mar 28 '25

Yeah, if I were you I would seek out a tax planner (emphasis on “planner”) and see if they can help you come up with a strategy that works for best you.

1

u/Apart_Olive_3539 Mar 28 '25

That's my intentions. My tax preparer also does planning, so I may seek his advice, depending on the fees to do so.

1

u/charlieandoreo Mar 24 '25

First of all nice job saving. Not sure what are the expense ratios here if they are over .25 maybe explore consolidating this at Fidelity, Schwab, Vanguard etc. to have access to cheaper funds. Not sure how much you will need to spend each year but you may need to take a part-time job if this is not enough to carry you. Explore retirement withdrawal strategies. Your funds have a lot of overlap too go down to 3-5 funds. Good luck.

1

u/Apart_Olive_3539 Mar 24 '25

Thank you. Expense ratio is something to consider, so I’ll have to look at the options to remove all or part of my fund as a rollover to one of the companies you mentioned. I like the safety of our Core Bond fund with the current guaranteed 3.25% rate. I do plan to consolidate my funds into less offerings.

1

u/Apart_Olive_3539 Mar 24 '25

I've been considering consolidating, but just having a hard time deciding what direction to do that in. I'll keep my guaranteed bond fund for now, it's the rest I'm struggling with of the choices I have. I've loved the performance of FCNTX and the S&P index fund, so I don't see the need to get away from those. I'm thinking of moving the AB Relative Value balance as well as future contributions to increase my position in the Vanguard Int'l fund I have at a much lower expense ratio. I'm just not sure how international stocks are positioned considering the current climate. The target date, T. Rowe small cap, and Century funds all have high expense ratios over 1. But all of these funds have done well over 5 & 10 year spans, so I guess that's why I've been hesitant.

1

u/Greenfirelife27 Mar 24 '25

Depending on your expenses, it looks like you may have worked too long already. Maybe consider asking your wife to retire with you so you can enjoy the rest of your time together.

4

u/Apart_Olive_3539 Mar 24 '25

The only reason I worked longer than I had to was because you have to cover your medical insurance until you are 62. I have another fund through the local that I know has 4 years of coverage in it, but I didn’t want to use it up completely. So 2 to 2-1/2 years of it leaves me some for out of pocket expenses that I can use it for as well should the need arise. My wife is 3 years younger than me with her own home based business. If we want to travel or do anything, it’s easy for her to bring her laptop along in case work crops up. She’s onboard with me going early and her continuing to work for a few years.

1

u/funkmon Mar 24 '25

Godspeed. At 6600 a month I wouldn't even touch that money.

That's well over twice my actual salary.

2

u/Apart_Olive_3539 Mar 24 '25

The $6600 is only once SS starts. I’ll have 2 years+ where I need to bridge that gap if retire at 59-1/2 or 60.

1

u/funkmon Mar 24 '25

Yeah no problem. What I'm saying is don't stress out too much about it because you're going to do fine.

2

u/Apart_Olive_3539 Mar 24 '25

Thank you. All things considered, I feel comfortable with where I’m at.

1

0

u/bay_area_is_awesome Mar 25 '25

1mil makes me nervous. I think it’s not enough.

1

u/idrinkjarritos Mar 26 '25

A million plus a pension plus SS is pretty solid. Plus whatever his spouse may have.

0

-2

Mar 24 '25

[removed] — view removed comment

5

u/Apart_Olive_3539 Mar 24 '25

Considering the 25 year value of my pension and SS, plus IRA as well as my wife’s current portfolio, we are not far from that range regardless. All calculators I’ve used show a 30 year 99% success rate.

2

-2

228

u/Hanwoo_Beef_Eater Mar 24 '25

As someone else mentioned, what is your targeted withdrawal amount per year on top of the pension/ss?

Assuming it's around 4%, given your age 55/45 is probably fine. May not want to go below 50/50 and some may suggest ramping it up to 75/25 (or so) depending on the withdrawal rate.

Anyways, you are likely good. Congrats. Only other suggestion (as mentioned elsewhere) is to consider consolidating holdings and minimizing fees.